Why Your HNW Client Keeps Delaying

Four Barriers and How to Break Them

There is a particular type of client meeting I have come to recognise over many years of practice. The client is intelligent, financially sophisticated, and genuinely concerned about the long-term security of their family. They understand exactly what they should do. They have been told what they should do, sometimes by multiple advisors, sometimes more than once. And they still have not done it.

Karan was one of those clients. He was 51 years old, the founder of a manufacturing group with operations across India, the UAE, and Vietnam. His net worth was approximately USD 30 million. He had two adult children, a deceased business partner whose estate had taken three years to settle, and, by his own admission, a financial plan that had not been reviewed in seven years.

When I asked him why nothing had changed in seven years despite clearly understanding the risks, he paused for a long time. Then he said: "Every time I sit down to think about this, I feel like I need to deal with the Vietnam expansion first, or the succession plan for the business, or the property refinancing. There is always something more urgent. And then another year has passed."

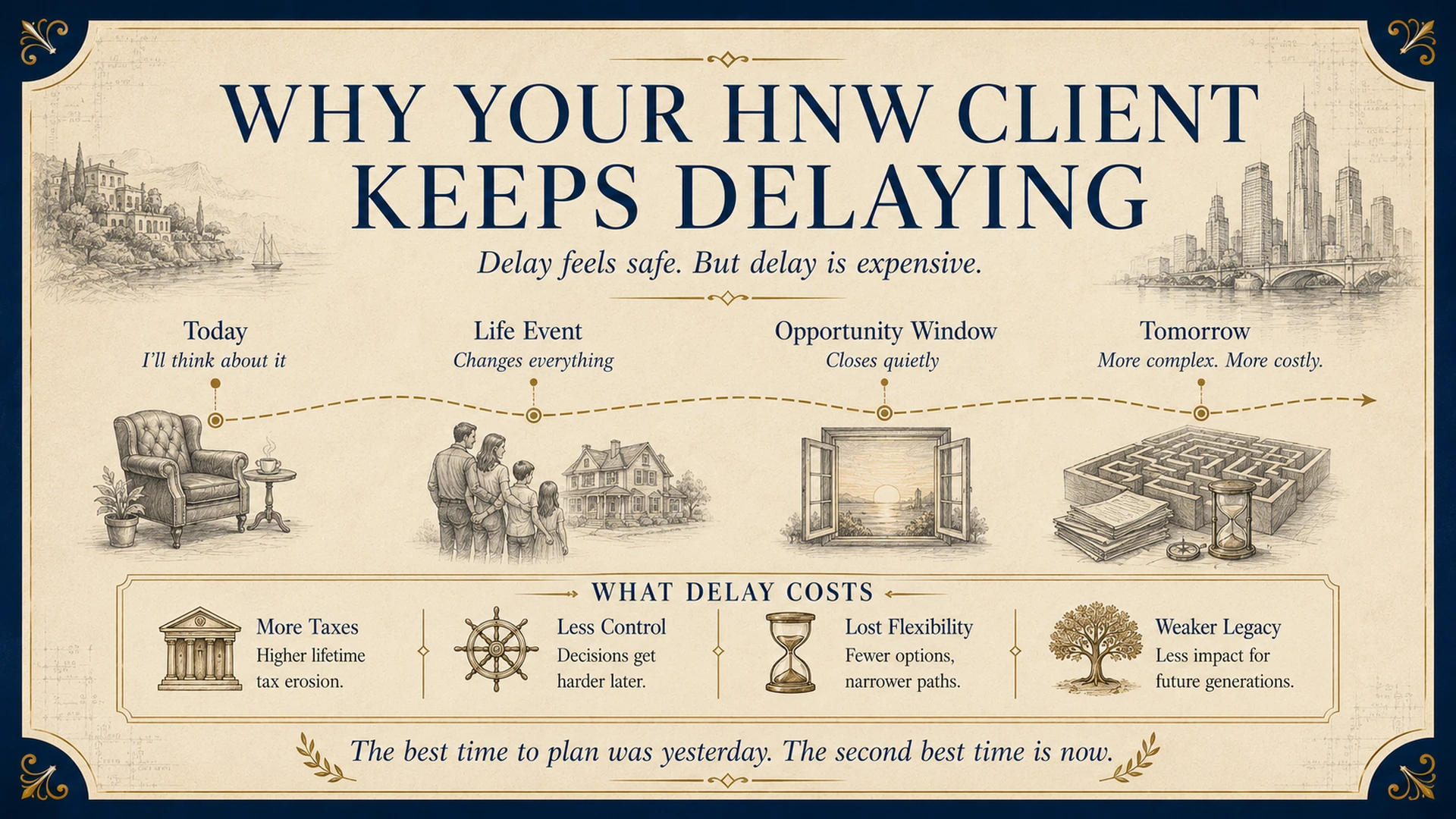

Karan was not unusual. In my experience, the gap between HNW clients knowing what they should do and actually doing it is the single most consistent feature of affluent wealth planning, across cultures, across geographies, across wealth levels. The problem is not knowledge. The problem is not resources. The problem is something more fundamental: a set of deeply rooted psychological barriers that make inaction feel reasonable, even responsible, in the moment.

This article names those barriers and gives financial planners specific, tested tools to break through each one.

Why Intelligent Clients Delay

Before examining the individual barriers, it is worth being precise about what kind of delay we are talking about. This is not the delay of disengaged clients who have never thought seriously about their financial future. The HNW clients who delay most persistently are often the most financially sophisticated people in the room. They understand compound growth, they understand estate tax, they understand the consequence of dying without a will. Their delay is not ignorance. It is a specific interaction between the complexity of the decisions they face and the psychological architecture of how they make choices under uncertainty.

The four barriers described below are drawn from more than two decades of direct practice working with HNW clients across Asia and the Middle East. They are not theoretical constructs, they are patterns I have observed consistently across hundreds of client relationships, and patterns that each have a specific, practical solution.

The Four Barriers: A Quick Reference

The table below summarises the four barriers, what they sound like from the client's perspective, and the intervention that breaks each one. The sections that follow examine each barrier in depth.

Table 1. The Four Barriers to HNW Planning Action. Each barrier has a distinct psychological root and a specific intervention.

Barrier One: Complexity Paralysis

The planning conversation for a genuinely wealthy client is not simple. It touches insurance, investment, tax, succession law, corporate structure, governance, and philanthropy, often across multiple jurisdictions simultaneously. When all of these dimensions are presented to a client as a single, interconnected problem that must be solved all at once, the most common response is cognitive overload followed by deferral. The client does not say "this is too complicated." They say "I need to think about this more", and then the year passes.

The solution is decomposition. Instead of presenting the full picture as one unified problem, break it into three sequential decisions: what needs to be protected immediately, what needs to be structured over the next twelve months, and what can be governed over a longer horizon. Each of these decisions is manageable. The combination of all three feels overwhelming.

I call this the "foundation first" approach, and I use a simple drawing to explain it. I draw a pyramid with three levels: the base (protection, insurance, liquidity, basic estate documents), the middle (structure, investment vehicles, tax efficiency, trust architecture), and the apex (legacy and governance, family constitution, philanthropic strategy, generational succession). I then tell the client that we cannot build the middle level before the base is solid, and we cannot build the apex before the middle is standing. This gives them a sequence. Sequences are actionable. Overwhelming problems are not.

The most common reason HNW clients delay planning is not that they are resistant. It is that they have been presented with a problem that feels too large to start. The advisor's job is to make starting feel small.

Barrier Two: The Advisor Maze

Many HNW clients arrive at a planning conversation already carrying the residue of conflicting advice. Their attorney recommended one trust structure. Their private banker recommended another. Their insurance broker proposed a policy that the tax advisor says creates a problem. Their accountant has opinions about all three. None of these advisors have spoken to each other, and the client has been left to arbitrate between expert opinions they are not equipped to evaluate.

The result is a particular form of paralysis that looks like procrastination but is actually a rational response to conflicting expertise. If your attorney and your tax advisor are giving you structurally incompatible recommendations, the sensible response is to wait, to hope that someone will eventually tell you which one is right. The problem is that nobody is ever asked to do this, so the client waits indefinitely.

The intervention here is to explicitly name the advisor maze and offer to navigate it. When I encounter a client in this situation, I say something like: "What you are describing is not unusual. You have multiple advisors who are each excellent in their domain, and they are giving you advice that is individually sound but collectively incoherent. My role here is not to be one more advisor with one more opinion. It is to take responsibility for the whole picture, to bring all of your advisors to the same table, establish your goals as the governing framework, and make sure every recommendation serves those goals rather than just its own domain."

This reframing almost always shifts the conversation. The client who was paralysed by conflicting advice is suddenly looking at someone who is willing to be accountable for the whole system. That accountability is extraordinarily rare in the wealth advisory world, and extraordinarily valuable to the client who has been living in the maze.

Barrier Three: Tomorrow's Certainty

The most persistent form of HNW planning delay is what I call "tomorrow's certainty", the conviction that the right time to act is just around the corner. When the business deal closes. When the market corrects. When the children finish university. When the property sale completes. When things settle down.

The insidious thing about tomorrow's certainty is that it is never demonstrably wrong in the moment. There usually is a deal closing. There usually is a market uncertainty. There are always things settling down. The client is not being irrational. They are making the entirely reasonable observation that the present moment feels like the wrong time to take on a large and complex planning exercise. What they cannot see, because nobody has shown it to them, is the cost they are paying for that reasonable-feeling decision.

The intervention is the present-value calculation. I do not argue with the client about whether now is a good time to plan. I calculate what each month of delay costs them in concrete financial terms. For a client with a USD 20 million investment portfolio earning 8 percent per annum in a taxable account, when a properly structured PPLI arrangement would eliminate the annual tax drag, each month of delay costs approximately USD 40,000 to USD 60,000 in foregone tax efficiency, depending on their jurisdiction. I write that number on a piece of paper and push it across the table.

This is not a scare tactic. It is the financial equivalent of making the invisible visible. The client who hears "you should plan your estate" is dealing with an abstraction. The client who sees "delay costs you USD 50,000 a month" is dealing with arithmetic. The conversation changes entirely.

Do not argue with a client's timeline. Calculate the cost of it. A concrete monthly number that the client can verify is more persuasive than any argument about urgency, because it shifts the conversation from opinion to arithmetic.

Barrier Four: The Good-Enough Trap

A significant number of HNW clients arrive with a pre-existing sense that their planning is already adequate. They have a will. They have some insurance. They have a company structure. They may even have a trust established some years ago. The combination of these elements creates a false sense of completeness, a feeling that the planning job has been done and does not need revisiting.

In most cases, this sense of completeness is significantly misplaced. The will was written in 2009 and does not cover assets acquired since then. The insurance sum assured was calibrated to income replacement when the client was 35 and is materially insufficient for the estate they now have. The trust was designed for a single-jurisdiction family and has never been updated to account for children who now live in three countries. The company structure that was efficient under the old tax regime is no longer optimal under the new one.

What the client is experiencing is the gap between a plan that existed and a plan that is current. These are not the same thing. A plan from seven years ago for a different set of circumstances is not "good enough", it is simply wrong in ways that have not yet become visible.

The intervention for the good-enough trap is not an argument. It is a live gap analysis conducted in the meeting. I take the client through five specific questions: Does your will cover all assets you currently own, in every jurisdiction where you own them? Is your life insurance sum assured sufficient to cover estate taxes and provide your family with genuine liquidity, not just income replacement? Are all of your policies trust-owned to prevent inclusion in the taxable estate? Has your family's jurisdictional footprint changed since your plan was last reviewed? Does every advisor you work with know what every other advisor has recommended? For the vast majority of clients who feel their plan is good enough, the honest answer to at least three of these questions is no. The gap analysis makes that visible without any argument being required.

Four Practical Interventions for Financial Planners

Understanding the barriers is the first step. Having a specific intervention ready for each one is what converts understanding into action, for the client and for the planner.

For complexity paralysis: introduce the pyramid structure in every initial engagement. Draw it. Show the client where they currently stand and what the next sequential step is. Make it clear that completing the base does not require solving the apex, and that beginning today with the most urgent layer is infinitely better than waiting until the whole picture is clear.

For the advisor maze: take the coordinating mandate explicitly. In the meeting, ask to be introduced to the other advisors. Offer to convene a shared briefing. The client who has been carrying the burden of conflicting expertise will almost always accept this offer with visible relief.

For tomorrow's certainty: calculate the monthly cost of delay before the next client meeting and present it as the opening item on the agenda. Do not present it as an alarm, present it as information. The client can choose to accept that cost. But they should do so knowingly.

For the good-enough trap: build the five-question gap analysis into your standard review process. Conduct it annually for every HNW client, not just those who express concern. Many clients who believe their plan is complete have never been asked these five questions explicitly, and the answers routinely surface material vulnerabilities.

The Conversation Behind the Delay

Karan, the client I described at the opening of this article, eventually did act. It took two meetings and a present-value calculation that showed him the cost of his seven-year delay in concrete terms he could not dismiss. The conversation that finally moved him was not about insurance or structures or tax. It was about the look on his face when he described what had happened to his business partner's family during the three-year estate settlement. He knew what the risk looked like. He had seen it. He just had not connected that knowledge to his own situation in a way that made action feel necessary.

That connection, between abstract knowledge and personal urgency, is what all four of these barriers prevent. And creating that connection, in the right way, at the right moment, is the most valuable thing a financial planner can do for a client who already knows what they should do.

The clients who need you most are not the ones who do not know. They are the ones who know and have not acted. Understanding why they have not acted is the beginning of being able to help them.

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.