The Rule That Makes Specialists Non-Negotiable

Most conversations about Private Placement Life Insurance focus on its advantages. Far fewer address the provision that governs what happens when a policy is structured incorrectly, and that provision is where the real risk lives.

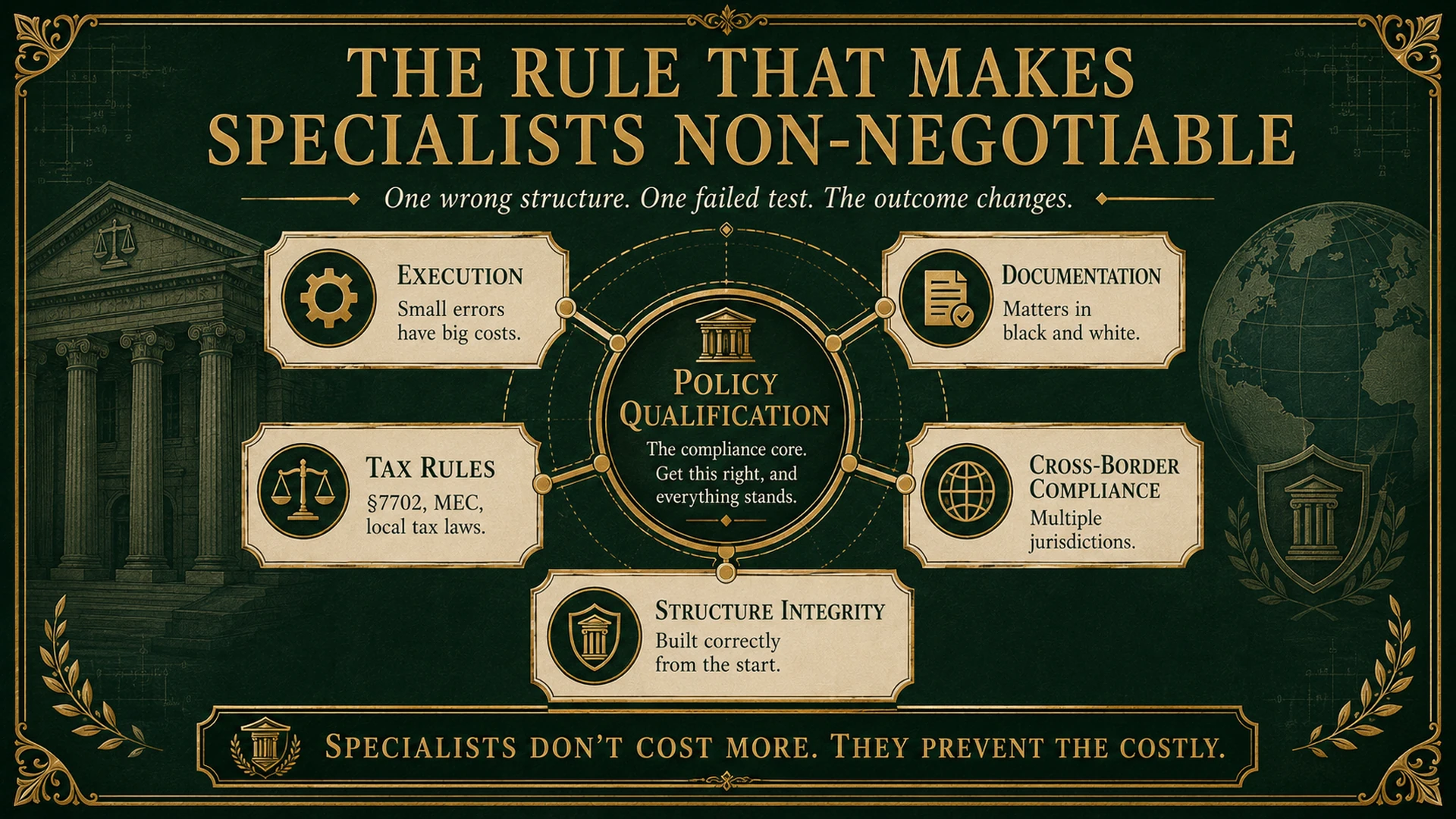

What §7702 does

IRC §7702 defines what qualifies as a life insurance contract for tax purposes. A contract must satisfy one of two actuarial tests, the Cash Value Accumulation Test or the Guideline Premium Test, to earn the tax treatment that makes PPLI valuable in the first place.

What §7702(g) does

If a contract fails those tests, §7702(g) steps in: the inside build-up is treated as ordinary income, taxable in the year it accrues, whether or not anything was withdrawn. A structure intended to be tax-deferred becomes fully taxable, and the entire economic rationale collapses.

Why this means specialists

Three things can trigger it, overfunding, a corridor violation, or a breach of the investor-control doctrine. None can be managed by a policyholder alone; each requires ongoing actuarial, legal and investment oversight. That is why the Tolani Flow® model builds §7702 compliance monitoring into the structure itself, rather than leaving it to chance. The enforcement reality does not weaken the case for PPLI, it is the reason specialist structuring is mandatory.

A §7702(g) failure does not make a policy underperform. It makes it fail entirely.

See how Tolani Flow® applies this → · Read the full research paper ↗

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.