Why 70% of Family Wealth Is Gone by the Second Generation, and How Financial Advisors Can Fix It

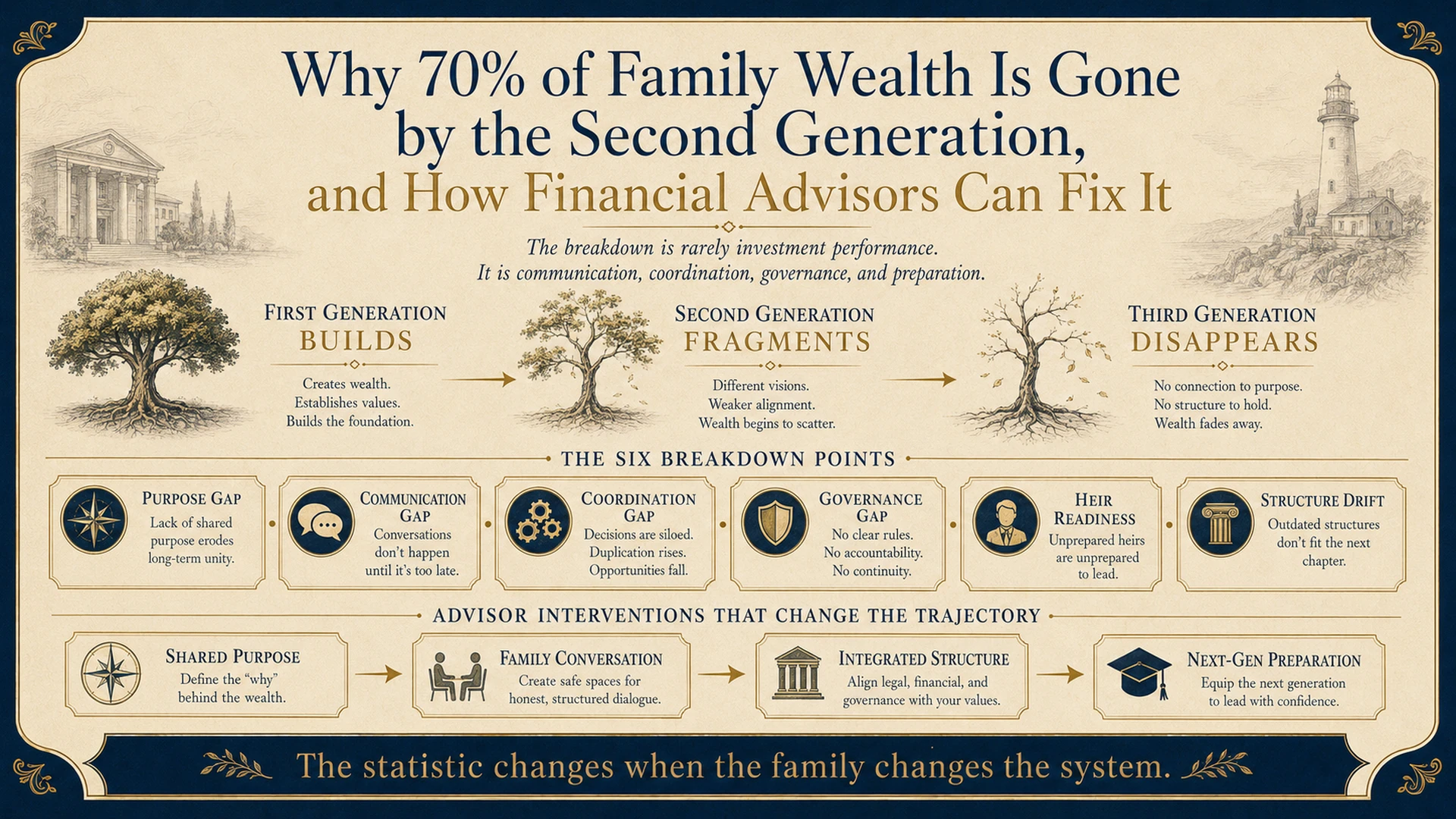

One of the most sobering statistics in wealth management is also one of the most consistently ignored: studies across multiple countries and generations of families have found that roughly 70 percent of family wealth is depleted by the second generation, and approximately 90 percent by the third. These are not numbers from a single study in a single market. They appear, with variations, across North America, Europe, Asia, and the Middle East, across different tax regimes, different cultural traditions, and different economic environments.

Most financial advisors know this statistic. Very few use it as the starting point for a client conversation. And almost none have a structured, practical response to offer when a client asks the obvious follow-up question: "Is my family going to be one of the 70 percent?"

This article answers that question, not at a theoretical level, but in the specific, actionable terms that a financial planner can use in the next client meeting.

Why Wealth Disappears: The Real Causes

The instinctive explanation for the 70-percent statistic is that the second and third generations are less hardworking, less disciplined, or less capable than the generation that built the wealth. This explanation is satisfying but wrong. Most second-generation heirs I have worked with are intelligent, motivated people who genuinely want to honour what their parents built. The problem is not effort or intelligence. The problem is preparation, or its absence.

Across decades of work with multi-generational families at the Tolani Family Office, we have identified three root causes that account for the overwhelming majority of generational wealth loss. They are not market losses. They are not tax bills. They are structural failures that accumulate quietly, over years, in the gaps between generations.

Unprepared heirs. The most common cause of generational wealth loss is heirs who inherit assets before inheriting the wisdom, values, and practical knowledge to steward them. This is not because families do not love their children. It is because preparing an heir for wealth is a deliberate, structured process that very few families ever undertake systematically. The patriarch who built USD 50 million from nothing knows, in his bones, how to manage money under pressure. His grandchildren, born into comfort, have never had to learn. The gap between those two experiences is where wealth is lost.

The generational skip. A related and widely underappreciated cause of wealth loss is what we call the generational skip, the transfer of wealth that bypasses one generation entirely, landing in the hands of a generation that has had no involvement in the decisions that shaped it. Grandparents, wanting to give generously and directly, skip the middle generation and transfer to the youngest. The result is heirs who inherit significant assets without the governance knowledge to manage them, a gap in institutional memory, and family dynamics tension as the skipped generation feels simultaneously excluded and relieved. The structural response is not to prevent grandparents from giving. It is to ensure that every transfer of wealth is also a transfer of context, values, and graduated responsibility.

No succession, only attrition. The third cause is perhaps the most preventable: families that have no explicit succession plan and wait for natural attrition, the death or incapacity of the patriarch, to trigger the transition. By the time this happens, the next generation has received no preparation, the governance structures are unclear, the family has accumulated years of unaddressed tension, and the transition itself becomes the crisis that reveals every structural gap that was never addressed.

Understanding Four Generations: A Framework for Advisors

One of the most practical tools I use with clients is what I call the generational landscape, a framework that maps the specific risk that each generation faces and the specific thing each generation needs. It gives financial planners a way to see the multi-generational challenge precisely, rather than as a vague concern about "the next generation."

Table 1. The Generational Landscape. Each generation's primary risk is different, which means the planning response must be generation-specific. Source: Author's framework from Tolani Family Office practice.

The most important insight from this table is that G1's primary risk is not the same as G3's or G4's. G1's risk is retention, holding on too long, failing to transfer knowledge and authority while they still have the energy and clarity to do it well. G2's risk is paralysis, waiting indefinitely for a permission to lead that may never explicitly come. G3's risk is entitlement, inheriting without earning the identity that comes from building something. G4's risk is disconnection, inheriting a story they have never been part of.

A financial planner who understands this framework can have a completely different conversation with each generation of the same family. The planning response for G1 is succession structure and knowledge transfer. The planning response for G2 is explicit authority and governance clarity. The planning response for G3 is graduated responsibility and values education. The planning response for G4 is the family story, expressed in ways they can connect with before the wealth arrives.

The Four Steps That Change the Outcome

The 70-percent statistic is not inevitable. It is a description of what happens in the absence of deliberate preparation. Across decades of working with multi-generational families, we have distilled the response to generational wealth loss into four concrete steps. They are not complex structures. They are disciplined commitments.

Table 2. The Four Steps to Generational Wealth Flow. These commitments address the four most common structural failure points in multi-generational family wealth. Source: Author's framework.

The Dimension That No Structure Can Replace: Heir Preparation

The four steps above are structural commitments. They provide the financial and legal foundation for generational wealth transfer. But the greatest risk to multi-generational wealth, as experience consistently shows, is not the structure. It is unprepared heirs.

Heir preparation is not financial literacy training. It is a comprehensive, developmental process with three distinct dimensions.

Financial literacy. Heirs need to understand how the family's assets work, how returns are generated, how the structures are designed, what the tax obligations are, how the governance system functions. This technical foundation should begin early, ideally in the mid-teens, and continue through structured participation in family council meetings and annual advisory reviews. The heir who sits in on the annual portfolio review for five years before inheriting it is not an expert. But they are not unprepared.

Stewardship values. Understanding why the wealth exists and what it is for cannot be taught through documents. It is transmitted through the family's story, its governance documents, its philanthropic programme, and, most powerfully, through direct mentorship by the founding generation. The grandfather who takes his granddaughter through the story of building the first warehouse is doing something no trust deed can replicate.

Graduated responsibility. Leadership capability, the ability to make decisions under uncertainty, navigate family dynamics, and represent the family's interests in complex situations, is developed only through practice. Small decisions first. Larger ones as capability is demonstrated. Full stewardship when readiness is confirmed, not when a birthday arrives. The Gupta family we worked with in 2023 had a designated succession leader in his late thirties who had never attended a family council meeting. He was not irresponsible. He was simply unprepared. We designed a two-year preparation programme, monthly conversations, graduated decision-making, structured participation in advisory reviews, that did not make him an expert, but ended his unpreparedness.

The most powerful question a financial planner can ask any multi-generational family is this: 'If something happened to the primary wealth creator tomorrow, would the first conversation between your heirs be about the person, or about the assets?' The answer tells you everything about heir preparation.

Four Practical Steps for Financial Planners

Map the generational landscape for every multi-generational family in your client book. Use the four-generation framework to understand which generation each family member belongs to, what their primary risk is, and what they specifically need. This mapping exercise, which takes no more than 30 minutes, transforms the vague concern about "the next generation" into a precise, generation-specific planning agenda.

Ask the one question that reveals heir preparation status: 'If the primary wealth creator became incapacitated tomorrow, would the designated heir know where everything is, understand the governance structure, and be able to work effectively with the advisory team?' A 'no' answer is the starting point for a two-year preparation programme, not a crisis response.

Introduce the four steps as a checklist in every annual review. For each of the four steps, life insurance, health coverage, education funds, retirement funds, rate the current completeness for every family member. The gaps that emerge from this checklist are almost always actionable immediately, and they provide a specific, practical agenda for the annual planning conversation.

Address the generational skip proactively. If you have a client family with three or more active generations, ask explicitly whether any transfer of wealth, gift, inheritance, or governance decision, has bypassed the middle generation. If so, the response is not to reverse the gift but to ensure that the skipped generation receives the governance context that should have accompanied it.

The 70 Percent Is Not Inevitable

The families that preserve wealth across generations are not the ones that got lucky or avoided all risk. They are the ones that had the conversations that most families avoid, about succession, about heir preparation, about what the wealth is actually for, about who has the authority to make decisions when the patriarch is gone. Those conversations are not easy. But they are exactly what a financial planner is positioned to facilitate.

The 70-percent statistic is a description of what happens without deliberate preparation. The financial planner who helps a family address the generational landscape, implement the four steps, and invest in heir preparation is not just providing financial advice. They are changing the trajectory of a family across generations, which is precisely the kind of value that creates relationships that last not for years, but for lifetimes.

The families that survive the shirtsleeves pattern are the ones whose advisors started the conversation early enough. That conversation starts with one question: how prepared is this family for the generation that comes next?

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.