What to Do When Your Client Has More Wealth Than Insurance Can Cover

The Progressive Wealth Utilization Framework for Financial Planners

Every financial planner who works with high-net-worth clients will encounter a moment that most training programmes never adequately prepare them for. The client sitting across from them has accumulated more wealth than any conventional insurance product can cover. The maximum insurable amount, USD 20 million, USD 50 million, even USD 100 million for the most sophisticated structures, represents a fraction of their net worth. And the question that the conversation inevitably raises is: what do you do with the rest?

This is not a niche problem. As HNW wealth has grown globally, and as families have accumulated assets across multiple jurisdictions and asset classes, the gap between what conventional insurance can address and what the client actually needs has widened significantly. The advisor who has no framework for this gap is not only failing to serve the client's full interest, they are at serious risk of being replaced by someone who does.

This article presents the Progressive Wealth Utilization Framework, a practical model for understanding how an advisor's value proposition must evolve as a client's wealth grows beyond the limits of conventional insurance, and what specific services fill the gap.

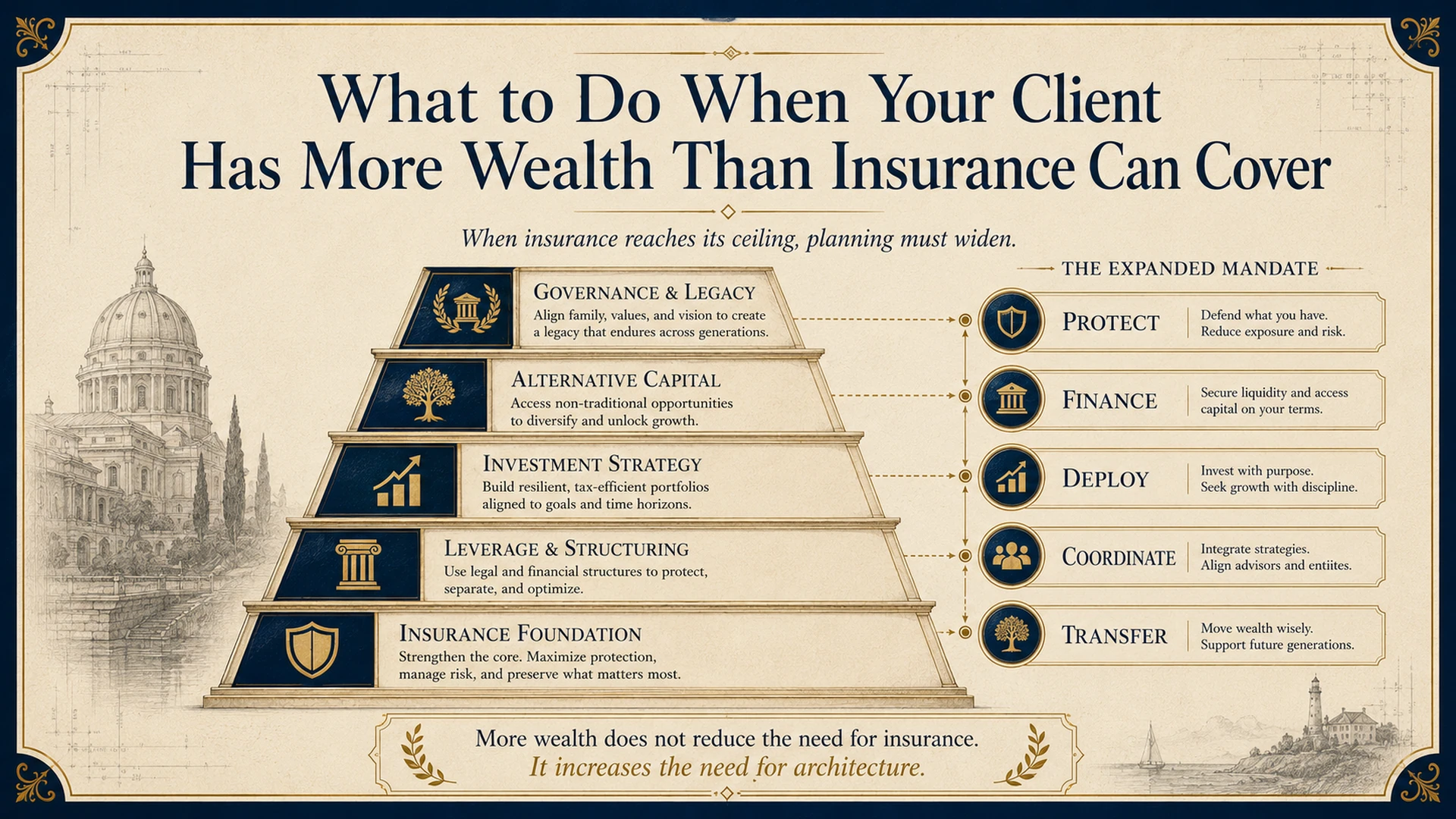

Understanding the Gap: Why Conventional Insurance Reaches Its Limit

Conventional life insurance, whether individual or premium-financed, has practical limits. In most markets, the maximum sum assured a single client can access through standard underwriting is in the range of USD 20 to 50 million, depending on their income, net worth, and jurisdiction. For premium financing structures and group solutions, this ceiling can be extended significantly. But even with extension, most ultra-high-net-worth clients have accumulated wealth that exceeds what any insurance structure can directly cover.

The conventional response to this limit is to treat it as the end of the insurance conversation, to note that the client has adequate protection and to move on. This is precisely the wrong response, and it is the point at which many advisors inadvertently cede the most valuable part of the client relationship to investment managers and private bankers who are willing to engage with the larger asset base.

The right response is to recognise that the limits of conventional insurance mark the beginning of a different kind of advisory conversation, one that addresses the wealth above the insurable threshold through a different set of tools and a different advisory mandate.

The Progressive Wealth Utilization Framework

The Progressive Wealth Utilization Framework is built on a simple insight: as a client's wealth grows beyond the limit of conventional insurance, the nature of the advisor's most valuable contribution shifts from protection placement to wealth architecture. The framework maps three levels of HNW solutions and the specific advisory function at each level.

Table 1. The Progressive Wealth Utilization Framework. As client wealth grows, the advisor's role shifts from protection placement to full wealth architecture and coordination. Source: Author's framework.

The most important insight in this framework is what happens at the transition from Level 2 to Level 3. At this point, the conventional insurance conversation begins to represent a smaller and smaller fraction of the client's total wealth. The advisor who does not evolve their proposition faces a genuine risk: the client begins to perceive them as relevant to only a fraction of their affairs, and begins to route the larger asset base to other professionals who engage with it directly.

The advisor who does evolve, who introduces PPLI as the tool that addresses the wealth above the conventional insurable threshold, and who positions themselves as the coordinator of the full wealth architecture, extends their relevance across the client's entire estate, not just the insured fraction.

As a client's wealth expands beyond the limits of insurable amounts, the traditional utility of an advisor may decrease unless they can provide additional value beyond traditional life insurance. The advisor who understands this proactively is the one who retains the full relationship.

AUA vs AUM: Understanding the Two Models Above the Insurance Threshold

Once the conversation moves above the conventional insurance threshold and into the PPLI and broader wealth architecture space, advisors typically operate in one of two modes, each with a different engagement model and a different compensation structure.

Asset Under Administration (AUA) is the model in which the advisor takes a coordinating and administrative role over the client's wealth structure without making the underlying investment decisions. In this model, the advisor implements and maintains the PPLI structure, coordinates the specialist team, ensures compliance and governance, and administers the client's asset organisation. The compensation is typically a fixed annual fee, a percentage of assets under administration, that provides a stable, perpetual income stream regardless of investment performance. For advisors who have built their practice on insurance and planning rather than investment management, the AUA model is typically the natural evolution.

Asset Under Management (AUM) is the model in which the advisor actively manages the investment decisions within the wealth structure, typically within a PPLI or family office mandate. The advisor makes or oversees the allocation decisions across the asset classes, and the compensation typically includes a performance component. This model requires genuine investment management capability. For most financial planners evolving from a protection and planning background, the AUA model is the more natural and immediately accessible expansion, it requires depth in PPLI structure, compliance coordination, and wealth architecture, which is precisely the expertise that insurance and planning advisors have already developed.

Practical Skills for the Expanded Mandate

Moving from Level 1 to Level 3 requires advisors to develop three practical skills that most protection-focused planning training does not address. These are not difficult to acquire, but they require deliberate effort and investment in specialist knowledge that goes beyond standard insurance licensing.

PPLI structure literacy. The PPLI conversation at Level 3 requires the advisor to understand, at a functional level, how PPLI structures work, the role of the policyholder, the underlying fund vehicle, the issuing jurisdiction, the compliance requirements, and the conditions under which the structure remains tax-efficient across residency transitions. The advisor who can explain which of three jurisdictions is optimal for this client and why is keeping the relationship. The advisor who defers that question to a specialist without being able to contextualise the answer is handing the most valuable part of the advisory mandate away.

Cross-jurisdictional awareness. UHNW clients with assets above the conventional insurance threshold almost always hold assets in multiple jurisdictions. The advisor who operates at Level 3 needs to understand, at minimum, the tax and compliance implications of the most common client jurisdictions, UAE, Singapore, UK, India, Switzerland, and the Cayman Islands, and know which specialist in their network to call for deeper analysis in each. This is not only about providing better advice. It is about asking better questions, the kind that reveal structural gaps that no single-jurisdiction advisor will ever see.

Compensation model confidence. One of the most common points at which the Level 3 conversation stalls is when the advisor cannot clearly articulate how they will be compensated for the expanded mandate. UHNW clients are sophisticated buyers. The advisor who presents the compensation structure clearly, my role is to coordinate your full wealth architecture across all specialist advisors and I charge an annual administration fee on assets under administration, is positioning themselves as a professional with a clear value proposition. Confidence in the compensation model is itself a signal of professional maturity that UHNW clients read accurately.

Four Practical Steps for Advisors Ready to Evolve

Map your client book for wealth above the conventional insurance threshold. Go through your top 20 client relationships and identify specifically how much of their net worth sits above the maximum amount you have conventionally insured for them. That uninsured and unstructured portion is the asset base your expanded proposition should address.

Introduce the three levels to every Level 1 and Level 2 client. Show them the framework. Explain that as their wealth has grown, there is now a portion of their estate that conventional insurance cannot directly cover, and that the same discipline they applied to the insured portion should be applied to the uninsured portion. This is not a new sale, it is the natural extension of the advisory relationship they already have with you.

Position PPLI as the structural bridge, not a product sale. The PPLI conversation at Level 3 is: here is the structure that addresses your wealth above the insurable threshold with the same discipline and efficiency that we applied to the wealth below it. The framing is architectural, not transactional.

Choose your model, AUA or AUM, before the conversation. Before introducing the expanded proposition to any specific client, be clear with yourself about which model you are proposing and why. Clients at this level will ask directly: what is your role, and how are you compensated? Having a clear, confident answer to that question is the difference between a conversation that moves forward and one that stalls.

The Advisor Who Grows With the Client

The most durable client relationships in financial planning are the ones where the advisor's value proposition has grown at the same rate as the client's wealth. The client who was first insured for USD 2 million and is now worth USD 200 million needs an advisor who has remained relevant across that journey, not by selling larger policies, but by evolving the nature of their contribution at each stage.

The Progressive Wealth Utilization Framework is the map for that evolution. It shows the advisor exactly when and how to expand the conversation, what tools address the wealth above each threshold, and what role the advisor should play at each level. The advisor who understands this framework and applies it proactively is not just a more useful advisor. They are an irreplaceable one.

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.