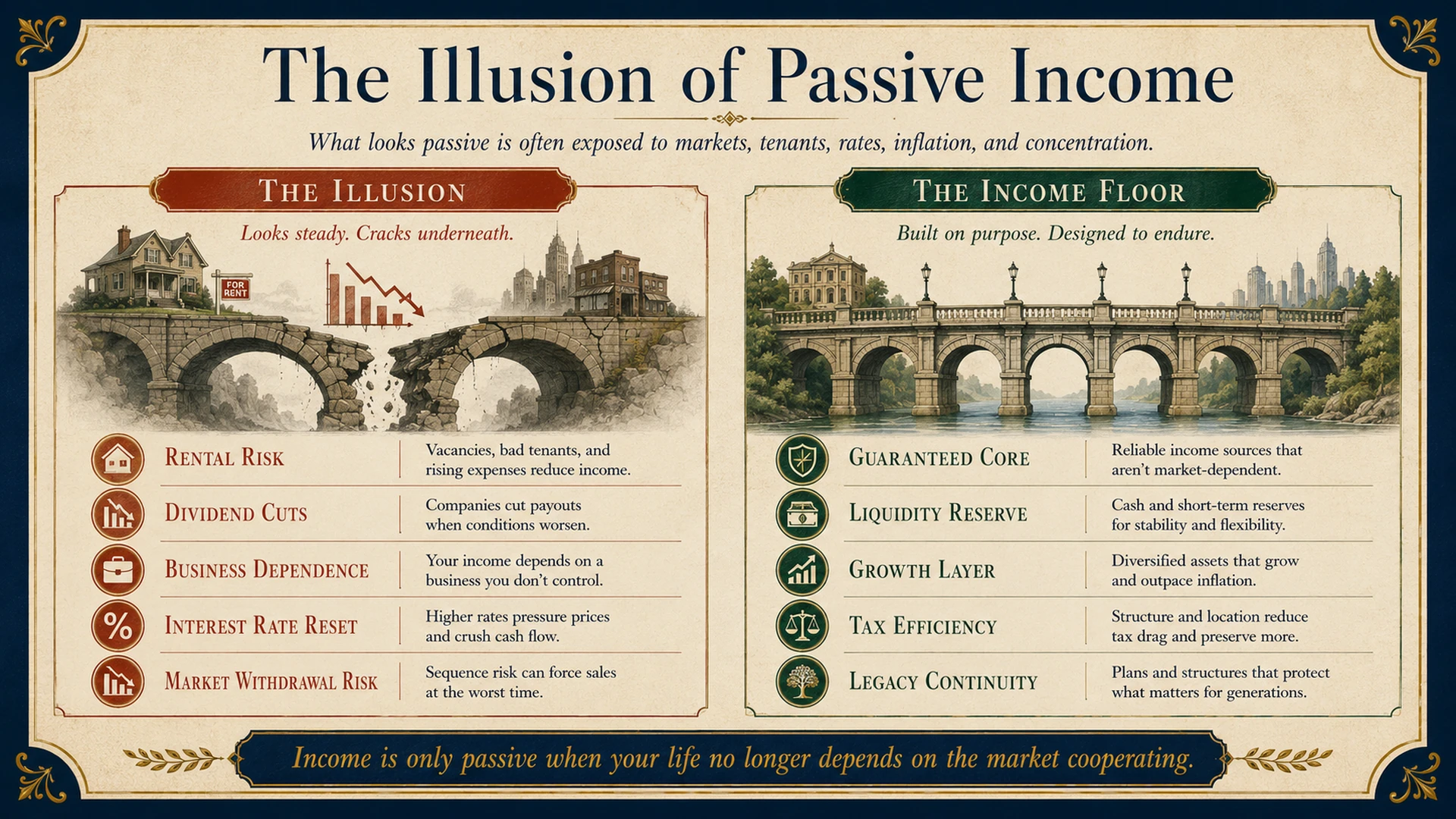

The Illusion of Passive Income

Building a Guaranteed Income Floor for HNW Clients

A client I worked with in Singapore, a 58-year-old businessman who had sold a significant portion of his manufacturing group five years earlier, described his situation to me with what he clearly felt was satisfaction: "I have passive income coming in from eight different sources. I am completely covered."

I asked him to walk me through the eight sources. He listed them: rental income from three commercial properties, dividends from a Singapore-listed portfolio, coupon income from a bond ladder, interest from fixed deposits, profit distributions from a minority stake in a private business, rental income from two residential apartments, and distributions from a family trust his father had established in the 1990s.

I let him finish. Then I asked: "Of those eight sources, how many are guaranteed, contractually, unconditionally, regardless of markets, regardless of tenants, regardless of corporate performance?"

He thought about it carefully. "None of them," he said finally. "Not really."

That realisation, that what most HNW clients call passive income is not actually passive, not actually guaranteed, and not actually an income floor, is the starting point for one of the most important planning conversations a financial planner can have. This article explains why the illusion of passive income is so widespread, why it matters, and what a genuinely guaranteed income floor looks like in practice.

Why 'Passive Income' Is Neither Passive Nor Guaranteed

The phrase 'passive income' has entered the financial planning vocabulary as shorthand for income that does not require the client to actively work for it. In that narrow sense, rental income, dividends, bond coupons, and fixed deposit interest are all passive, they arrive without the client trading their time. But passive is not the same as guaranteed. And for the purpose of retirement planning for HNW clients, guaranteed is the only thing that matters.

Consider each of the six most common sources of income that HNW clients rely upon, and what is genuinely true about their reliability.

Rental income is one of the most psychologically reassuring forms of income, because the underlying asset, bricks and mortar, feels permanent. But rental income is dependent on tenants, on market conditions, on property maintenance cycles, on jurisdictional rent control legislation, and on the client's ability to manage the property actively or fund its management passively. A commercial property without a tenant produces no rental income. A residential apartment requiring a major renovation produces cash outflows, not inflows.

Bond coupon income is more predictable than rental income, but it is subject to reinvestment risk at maturity, to the credit quality of the issuer, and to the yield environment prevailing when the bonds are rolled over. A client who locked in 6 percent coupons in 2019 faces a very different income stream upon reinvestment in a lower-yield environment.

Fixed deposit interest carries the same reinvestment risk and the additional limitation of fixed durations that reduce flexibility. Inflation erosion means that even if the nominal income is consistent, its purchasing power may decline significantly over a decade.

Dividend income is structurally variable. Dividends depend on corporate performance and board decisions that are entirely outside the client's control. Companies cut or suspend dividends in precisely the conditions, market downturns, business stress, when the client most needs income stability.

Government pensions and social security are the most reliable guaranteed income source for most retirees. But for globally mobile HNW clients, the UAE resident, the Singapore investor, the international entrepreneur with multiple residencies, there is frequently no meaningful state pension entitlement in their country of residence. They have, in effect, opted out of the system that provides the income floor for most of the population.

Annuity or endowment income is the only genuinely controllable income stream in the list. It is the one source whose payment is contractually guaranteed by the issuing insurer, for a fixed term or for life, regardless of market conditions, corporate performance, or the behaviour of any third party. It is the only source where the client can say, with precision: 'On the fifteenth of every month, this amount will arrive.' And it is the most underused source in the income planning of almost every HNW client I encounter.

The Six Sources: A Framework for Every Income Audit

At the Tolani Family Office, we audit every client's income structure against six categories. The goal is not to have all six, it is to have a deliberate, documented mix in which the guaranteed sources cover the client's baseline lifestyle needs, and the variable sources fund growth, lifestyle enhancement, and philanthropy. This is what we call the hybrid income strategy.

Table 1. The Six Sources of HNW Income, Reliability and Planning Considerations. Source: Tolani Family Office income audit framework.

When the cash flow is certain, the family conversations change. They stop being about survival and start being about purpose., Dr. Sanjay Tolani

What a Genuine Income Floor Looks Like

A genuine income floor has one defining characteristic: it cannot be disrupted. Not by a market crash, not by a tenant vacating, not by a corporate board cutting the dividend, not by a rate cycle turning, not by a family emergency that requires urgent liquidity from other assets. It arrives, unconditionally, every month.

For most HNW clients, building a genuine income floor means sizing and structuring an annuity before any other income planning is done, not as an afterthought or a supplement, but as the foundation. The practical sizing question is: what is the minimum monthly income the client's family needs to maintain their baseline lifestyle standard, and how much annuity capital is required to fund that income for life?

The calculation is not complex, but it is one that most clients have never done. Take a client whose family requires USD 20,000 per month to maintain their lifestyle at its current standard, without drawing on investment capital. A whole-of-life annuity providing USD 20,000 per month for a 58-year-old male in a well-regulated insurance jurisdiction typically requires a single premium of approximately USD 3.0 to 3.5 million, depending on insurer, jurisdiction, and annuity terms. That premium, once placed, produces a monthly income that cannot be disrupted by anything outside the insurer's solvency, which is why insurer credit rating and jurisdictional regulation matter more in this decision than in almost any other insurance placement.

Once the floor is in place, the variable income sources, rental income, dividends, bond coupons, serve a different and less pressured role. They fund the lifestyle above the baseline, the investment portfolio growth, and the philanthropic programme. And crucially, because the client's survival needs are covered unconditionally, they can manage the variable sources with patience and judgment rather than anxiety. A commercial property without a tenant is a short-term irritation, not an existential threat, when the USD 20,000 is already arriving every month.

Why Globally Mobile HNW Clients Need This Most

For the standard domestic retiree in a developed country, the state pension provides a partial income floor that underpins all other retirement income planning. The globally mobile HNW client, the UAE resident with no state pension entitlement, the international entrepreneur who has lived and worked in five countries without accumulating meaningful pension rights in any of them, the family office principal who exited the employment system decades ago, has no such floor.

For this client, the annuity is not a supplement to a state pension. It is the state pension that the client must build for themselves. This reframing changes the urgency and the scale of the conversation significantly. It is not a question of whether to buy an annuity. It is a question of whether the client has yet built the income floor that every other retirement plan in the world takes for granted.

The jurisdictional considerations for globally mobile clients add further complexity. The annuity issuer must be regulated and rated in a jurisdiction whose insurance regime the client's various countries of residence will recognise for tax purposes. Luxembourg, Singapore, and the UAE are the three most commonly used domiciles for GCC and Asian clients, each with different regulatory strengths, different treaty networks, and different requirements for portability across residency transitions.

Three Practical Steps for Financial Planners

Conduct a guaranteed income audit for every HNW client in your book. Go through each client's income structure and identify explicitly which sources are contractually guaranteed and which are market or third-party dependent. For most HNW clients, the proportion of guaranteed income is either zero or covers only a fraction of baseline lifestyle needs. Present this gap as a specific financial number, the dollar amount of monthly income that has no floor under it, rather than a general observation about income diversification.

Size the income floor before sizing anything else. Before any investment allocation conversation, before any PPLI structure discussion, before any estate planning work, ask: what is the minimum guaranteed monthly income this client's family needs, and is it funded? If not, this is the first planning priority, not the last. The floor must be built before the portfolio can be managed with the composure and patience that genuine long-term wealth building requires.

Frame the annuity as the missing asset class, not as a product. Most HNW clients have a mental model of their income as a portfolio, a diversified mix of sources that, taken together, provides income security. The conversation that works is not 'would you like to buy an annuity?' It is 'of your current income portfolio, what percentage is contractually guaranteed regardless of external conditions?' The answer to that question creates the opening for the annuity as the one allocation that makes the rest of the portfolio genuinely resilient.

The Income That Changes Everything

My Singapore client, the one with eight sources of passive income and a guaranteed floor of zero, spent about six months after our first meeting resisting the annuity conversation. He had spent a career generating returns. The idea of converting capital into a fixed income stream felt like defeat, like admitting that his investing days were over.

What changed his mind was not a number. It was a scenario. I asked him to imagine that two of his three commercial properties were vacant simultaneously, the private business had suspended distributions for a year, and his dividend portfolio had been cut by 40 percent due to a market correction. In that scenario, which was not extreme, merely the kind of thing that had happened in every decade of the previous century, what was his guaranteed monthly income? The answer was somewhere between USD 4,000 and USD 6,000. His family needed USD 22,000.

The gap between USD 6,000 and USD 22,000 is not a theoretical risk. It is a specific number that describes what happens to a family's lifestyle in a genuinely bad year. The annuity that closes that gap is not a product. It is the piece of the income structure that allows every other piece to fulfil its purpose without anxiety.

The financial planner who helps a client see this, and build the floor before the bad year arrives, is doing the most practically important work in retirement planning.

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.