The Four C's of Wealth Preservation

What Every Advisor Should Audit Before Anything Else

My father had a small office in a building full of families waiting to tell him things they had not told anyone else. I was young when I began sitting quietly outside that office, listening to the conversations that drifted through the door, conversations about businesses that had been built over lifetimes and were now in dispute, about property nobody could access because the documents were in a drawer in a house nobody could enter, about children who could not agree on anything except that something had gone wrong.

One evening, after a particularly long day, my father sat beside me and said something I have carried for decades: "Wealth does not destroy families. Unprepared families destroy wealth."

I have spent the better part of my career understanding what he meant. And the conclusion I have reached, through hundreds of family engagements across the GCC, Southeast Asia, and South Asia, is this: the families that preserve wealth across generations are not smarter, luckier, or richer than the families that lose it. They simply have four habits that the others do not. At the Tolani Family Office, we call them the Four C's of Wealth Preservation.

This article explains what they are, why they matter, and, most importantly, how financial planners can use them as the foundation of every client engagement, before any product is recommended, before any structure is designed, and before any strategy is proposed.

Why Wealth Disappears, and Why It Is Never the Reason You Think

There is a saying repeated across cultures, in languages I have heard from Tokyo to Lagos to Dubai: shirtsleeves to shirtsleeves in three generations. The first generation builds in shirtsleeves. The second generation grows up in comfort. The third generation spends the inheritance. By the time the fourth arrives, the ocean that once felt endless has quietly, invisibly shrunk.

Most people assume this pattern reflects a failure of character, that the second and third generations were less hardworking, less careful, less committed to the family's values. In my experience, this is almost never true. Most heirs are intelligent, caring people who genuinely want to honour what was built. The problem is not character. The problem is what I have come to call the silent leaks.

Silent leaks do not announce themselves. They are taxes that arrive at the worst possible moment, not because they were unavoidable, but because planning was not done early enough. They are assets scattered across countries and accounts and entities, making oversight fragmented and vulnerability widespread. They are children who inherit assets before inheriting wisdom, overwhelmed by responsibility they were never shown how to carry. They are legal structures that are weak or outdated, causing delays and disputes and costs that drain what decades of effort built. And they are a world that moves faster than planning, through inflation, shifting laws, and global uncertainty.

None of these leaks feel urgent in the moment. None of them announce themselves. Together, they quietly erode the ocean that families spent decades building. Wealth disappears slowly, and then suddenly.

The Four C's are the practical framework that plugs these leaks. Not by creating complexity, but by building the habits that prevent the leaks from forming in the first place.

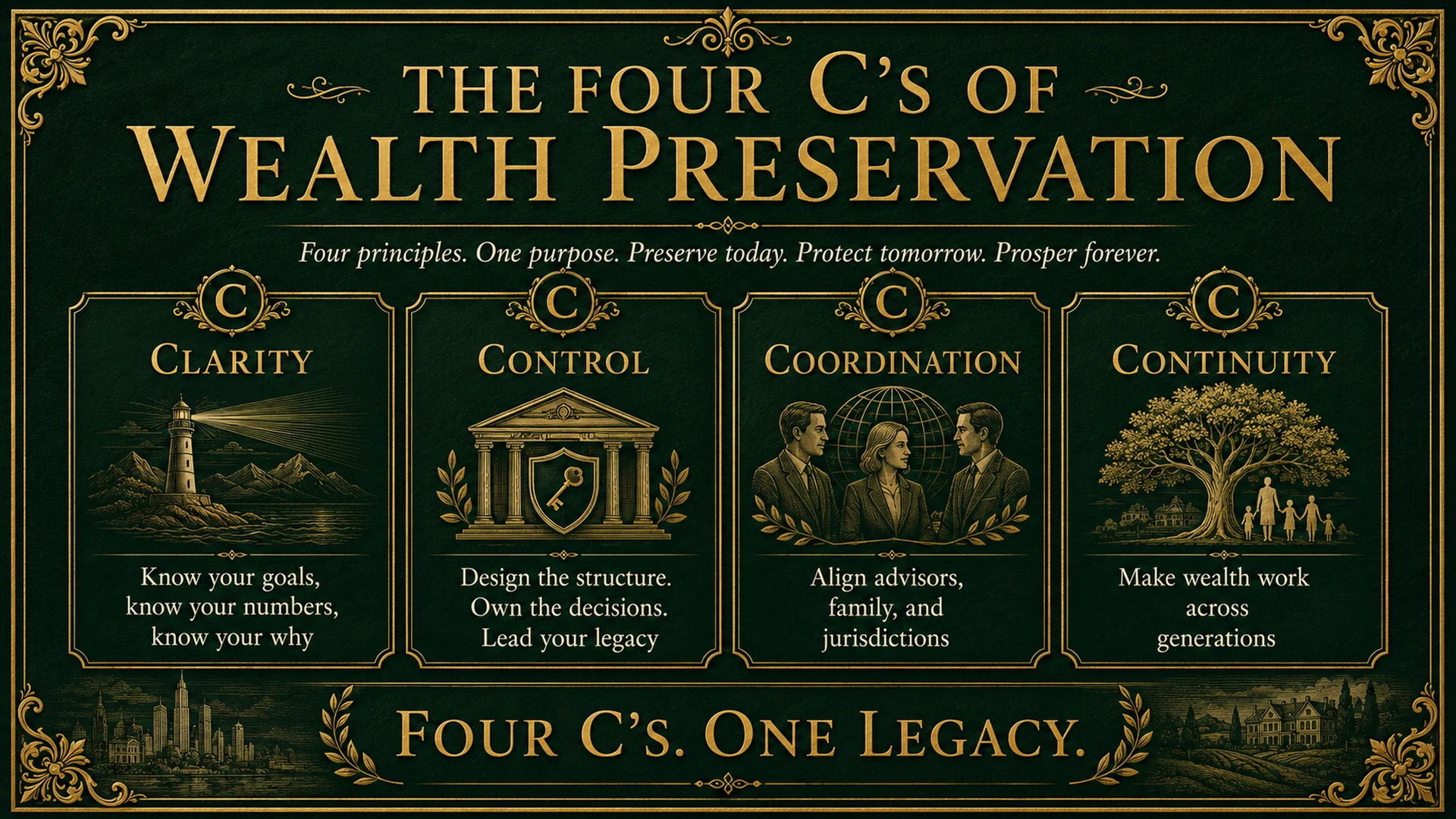

The Four C's: A Framework for Every Client Audit

The Four C's are not products. They are not structures. They are diagnostic habits, questions that every financial planner should ask of every HNW client, in this sequence, before any planning conversation moves to product selection or investment strategy.

Table 1. The Four C's of Wealth Preservation. These are diagnostic habits, not product categories. Every HNW client engagement should begin with a Four C's audit before any strategy or product is discussed.

The Cost of Skipping the Audit: The Mehta Lesson

Rajiv Mehta built Mehta Logistics from a single warehouse at age twenty-six to one of the largest privately held freight and warehousing businesses in South Asia, with operations extending into the Gulf, East Africa, and Southeast Asia. By 2019, the Mehta family's consolidated net worth stood at approximately USD 140 million, logistics group, commercial real estate in Mumbai, Dubai, and Nairobi, a residential portfolio across London and Singapore, and a charitable foundation focused on rural education.

From the outside, this was a picture of generational success. From the inside, it was a family sitting on a structural fault line they could not see.

When Arjun, Rajiv's son, came to our office, he arrived with one question: "If something happened to my father tomorrow, what would actually happen?" The answer, as we pieced it together, was not comfortable.

The Singapore equities portfolio had no named beneficiaries and sat in a jurisdiction where probate takes 18 to 36 months. The Dubai commercial properties were co-registered with a former business partner under an arrangement not legally reviewed in eleven years. Arjun and Priya, his sister, held no documented shareholder agreement and had never formally discussed succession, valuation, or control. There was no liquidity structure, no life insurance, no PPLI, no credit facility, that could provide immediate cash flow in a transition. Rajiv's will had not been updated since 2009.

Running the Four C's audit on the Mehta family took less than two hours. The findings covered all four dimensions: confidentiality had been violated by a business partner who knew the full extent of the family's holdings; consolidation was absent because nobody could produce a single current inventory; control was nonexistent because the structures that should have protected Rajiv's intentions were missing or outdated; and continuous flow was impossible because there was no mechanism to move wealth across the transition without court involvement.

The remediation took eighteen months. What it required, legally, structurally, and financially, was a fraction of what it would have cost had the family arrived at a transition event without it. The lesson is not about the Mehtas specifically. It is about how many clients are sitting in your office right now with the same invisible fault lines and no idea they are there.

The Four C's audit is not a product conversation. It is the conversation that earns the right to have every product conversation that follows. Advisors who begin with the audit build relationships that last generations.

How to Use the Four C's Audit in Your Practice

The Four C's are most valuable as the standard opening framework for every new HNW engagement, and as the annual review structure for every existing client relationship. The audit takes approximately 90 minutes in a first meeting and 30 minutes in annual reviews. It produces four outputs: a clear picture of the current state of each C, a prioritised list of the vulnerabilities that need addressing, a sequence for addressing them, and a coordinating role for the financial planner that is explicitly separate from any product recommendation.

Confidentiality audit: Ask the client who currently has access to information about their wealth, family members, advisors, business partners, banks, government agencies. For each category, ask whether that access is intentional, documented, and appropriate. The planner who asks these questions is rarely the first advisor to sit across from the client, but they are almost always the first to ask this question, which establishes an immediate differentiation.

Consolidation audit: Ask the client to describe everything they own, in every jurisdiction, with its current legal ownership structure. Most HNW clients cannot do this from memory. The gaps and uncertainties that emerge from this exercise are almost always the most productive part of the first meeting, because they are the areas where structural drift has accumulated without anyone noticing.

Control audit: Ask five specific questions: Is there a current will covering all assets in all jurisdictions? Is there a lasting power of attorney in place? Are all policies, trusts, and investments correctly titled? Is there a shareholder agreement covering the business interests? Has any structure been reviewed in the past three years? A 'no' answer to any of these is a gap that needs addressing before any new planning layer is added.

Continuous flow audit: Ask one question, if the primary wealth creator died or became incapacitated tomorrow, what would happen in the first 72 hours, the first month, and the first year? Walk through the answer together. The parts of the answer where the client says 'I'm not sure' are the parts where continuity planning is absent.

Structure Is the Planning

The most important insight my father's clients taught me, and that decades of my own practice have confirmed, is this: the families that preserve wealth are not the ones with the best investments. They are not the ones with the lowest tax rates. They are not the ones who got lucky in their markets. They are the ones who built structure before they needed it, who had the conversations about control and continuity before a crisis forced those conversations in the worst possible conditions.

The Four C's give financial planners a framework to have those conversations proactively, professionally, and in a way that positions the planner as a genuine strategic partner rather than a product provider. The advisor who audits every client against the Four C's at the start of every engagement is doing something that very few advisors do, and providing a service that no investment return can replicate.

Numbers create money. Structure creates peace. The Four C's are how you build the structure.

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.