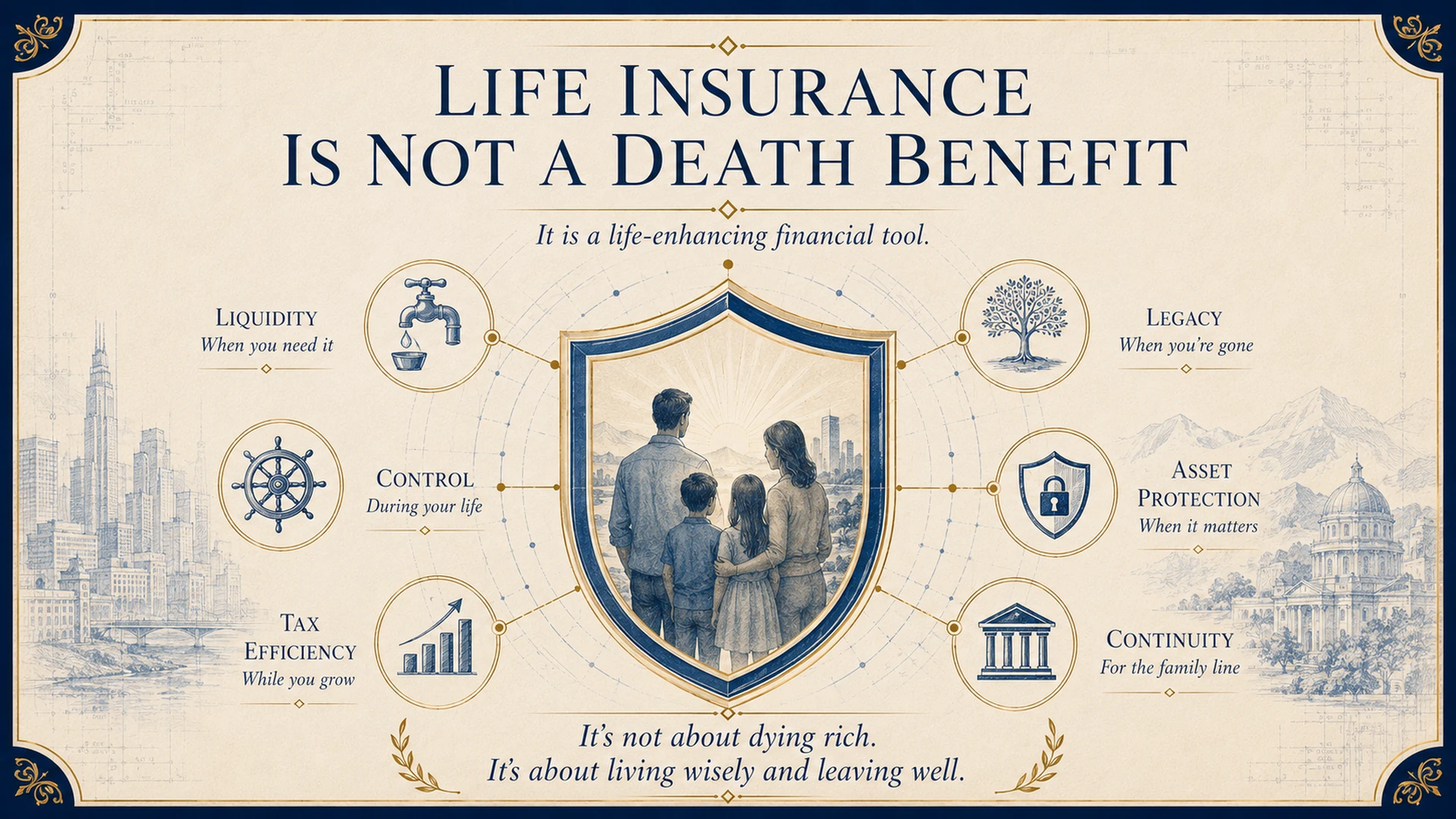

Life Insurance Is Not a Death Benefit

Reframing the Conversation for HNW Clients

I want to describe a moment that changed how I think about the life insurance conversation entirely.

I was sitting across from a client, a 56-year-old technology entrepreneur with a net worth of approximately USD 40 million. He had a sophisticated investment portfolio, a family office structure in Singapore, and a deep scepticism about life insurance. He had spent most of his career building assets. He was not, in his own words, interested in products that paid out when he died.

I did not argue with him. Instead, I asked him one question: "What percentage of your current portfolio is guaranteed, not likely to appreciate, not historically stable, but contractually guaranteed regardless of what markets do?"

He thought for a moment. "Very little," he said. "Almost none, if I'm honest."

"That," I told him, "is the gap I am here to discuss. Not how to protect your family if you die. How to guarantee a portion of your portfolio and transfer it to your children at the exact moment they need it, in the exact amount you decide, with zero exposure to the probate process, the tax system, or the timing of the markets."

That conversation lasted two more hours. It ended with a planning engagement. Not because I changed his mind about life insurance, I never mentioned those words again. I simply showed him a problem his portfolio had, and a solution that happened to be structured as an insurance contract.

The reframe is the conversation. This article explains how to make it.

Why the Standard Insurance Conversation Fails with HNW Clients

The conventional life insurance conversation is built for a specific client profile: a working professional with dependents and an income that their family cannot afford to lose. The conversation is essentially one of income replacement, if you die, your family will need money, and this policy provides it. That is a legitimate and valuable service for the right client.

It is the wrong conversation for a high-net-worth client who has already won the income game. When a client has USD 30 million in assets, they are not worried about income replacement. Their family will not be destitute if they die. What they are worried about, though they may not use these words, is disruption. Specifically:

Disruption to the transition of their estate, which may sit in probate for years if it is not properly structured.

Disruption from unexpected tax liabilities that force the sale of assets at the wrong time and at the wrong price.

Disruption from the absence of immediate liquidity at precisely the moment, the first six months after death, when their family most needs to be making clear-headed decisions rather than scrambling for cash.

Disruption to the business or investment portfolio that cannot continue operating at full capacity during a prolonged, contested estate process.

None of these concerns are about income replacement. They are about portfolio composition, estate engineering, and structural certainty. And yet most life insurance conversations are still presented in the income replacement frame, which is why most HNW clients mentally file insurance under "products for people who need protecting" and exclude themselves from the conversation before it has begun.

The HNW client who says 'I don't need life insurance' is not wrong about their situation. They are wrong about what life insurance, properly structured, actually does.

The Three Functions of Life Insurance at the HNW Level

When I work with HNW clients, I describe life insurance as having three distinct functions that operate simultaneously. The advisor who understands and can articulate all three is having a fundamentally different conversation from the advisor who presents insurance as protection.

Function one: immediate liquidity at the moment of maximum need. The greatest financial vulnerability in most HNW estates is not the size of the estate, it is the timing of access. Investment portfolios may take weeks or months to liquidate. Real estate may take a year or more. Business assets may take years and may require sale at a discount to achieve settlement. In the meantime, the family needs cash: to pay estate duties, to fund the operating costs of a business in transition, to meet the day-to-day needs of multiple households, and to retain the professional advisors who will manage the estate settlement process.

A properly structured life insurance policy, held in trust to ensure it sits outside the taxable estate, provides a cash payment to the family within days of death, with no probate process, no tax exposure, and no dependence on market conditions or asset liquidity. For a family with USD 40 million in largely illiquid assets, a USD 5 million policy provides a financial bridge that changes the entire character of the transition from a crisis into a managed process.

Function two: guaranteed capital certainty in an uncertain portfolio. Every sophisticated HNW client understands that their portfolio carries market risk. The equity positions can fall. The property can be illiquid. The private equity is locked up for years. In the context of a portfolio that is overwhelmingly exposed to market and liquidity uncertainty, a structured whole-life or endowment allocation serves a specific portfolio function: it provides a guaranteed capital value that is contractually protected regardless of external conditions.

I present this to investment-oriented clients using a framing they immediately recognise: put option logic. A put option provides a floor, a guaranteed minimum outcome regardless of how the underlying asset performs. You pay a premium for that certainty. The premium is the cost of removing tail risk. Whole life and endowment structures are the put option on the wealth creator's most important asset: their life and the capital it represents. The structure provides a guaranteed floor, always in-the-money, with a death benefit that reflects the full insured value at the moment it is triggered.

Function three: structural estate transfer with no court involvement. In most jurisdictions, assets that pass through the estate are subject to probate, a court-supervised process that is public, time-consuming, expensive, and subject to challenge. For HNW families with assets in multiple countries, probate is not one process but potentially several simultaneous processes operating under different legal systems. The result is that the family's access to wealth is delayed by years, and the cost of access, in legal fees, in lost investment opportunity, in family stress, can be enormous.

A life insurance policy with named beneficiaries passes entirely outside the estate and outside the probate process. The death benefit goes directly to the named beneficiaries, who need not be the legal heirs, without court delay, without public disclosure, and without legal contest. For a family that has spent decades building wealth across multiple jurisdictions, this is not a peripheral feature. It is the difference between an estate transition that takes eighteen months and one that takes a fortnight.

The Language Shift That Opens the Conversation

The reframe is not just conceptual. It is linguistic. The words that open the HNW insurance conversation are entirely different from the words that open the standard protection conversation. The table below shows the specific shifts that move the conversation from a product sale to a strategic planning discussion.

Table 1. The Language Shift for HNW Insurance Conversations. The left column closes the conversation before it begins. The right column opens a strategic planning discussion.

The linguistic shift matters because HNW clients make rapid, intuitive judgements about whether a conversation is relevant to them. The moment they hear income replacement language, they categorise the advisor as someone who is selling protection products to people who need protecting, and they mentally step outside that category. The portfolio language keeps them inside the conversation long enough to engage with the actual substance.

The Question Financial Planners Ask Wrong

The standard insurance sizing question is: "How much do you need?" For HNW clients, this is the wrong question, and it is why so many of them are significantly under-covered relative to the problems their estate will face.

The question I ask instead is: "How much disruption can your family absorb?"

These are different questions with different answers. "How much do you need" points toward income replacement calculations, ten times earnings, or the present value of future income. These are legitimate metrics for a client whose family depends on their earned income. They are irrelevant for a client whose family will not depend on earned income regardless of what happens.

"How much disruption can your family absorb" points toward something entirely different. It asks: what is the tax liability on this estate, and is there cash to pay it without a forced sale? What is the value of this business in the twelve months following the founder's death when clients may leave, staff may be uncertain, and a sale process may be forced? What is the cost of eighteen months of probate delay on a portfolio that should have been compounding at 8 percent? What is the liquidity gap between the moment of death and the moment the estate settles, and can the family live comfortably inside that gap?

These questions typically produce a much larger figure than the income replacement calculation, and a much more honest one. The USD 40 million entrepreneur I described at the opening of this article needed not a USD 5 million income replacement policy but a USD 15 million liquidity and estate certainty structure. The difference was the question I asked.

Three Practical Steps to Reframe the Conversation in Your Practice

Begin with the portfolio gap question, not the protection question. In every HNW engagement, before any insurance product is mentioned, ask: "What percentage of your current portfolio is contractually guaranteed regardless of market conditions?" This question forces the client into a portfolio thinking frame, reveals a genuine gap in almost every sophisticated portfolio, and creates the opening for insurance as a structural solution rather than a protection product.

Present the three functions, not the single function. Most financial planners present life insurance as performing one function: death benefit. Present it as performing three simultaneously: immediate liquidity, guaranteed capital certainty, and probate-free estate transfer. The three-function frame positions the policy as an integrated portfolio tool that addresses multiple planning problems at once, which is exactly what a well-structured HNW policy does.

Change the sizing question. Replace "how much coverage do you need?" with "how much disruption can your family absorb?" Walk through the estate disruption calculation with the client: the tax liability, the business continuity gap, the probate delay cost, and the liquidity gap. The number that emerges from this calculation is almost always larger than the income replacement figure, and it gives the client a concrete reason to own a larger policy that they can verify for themselves.

The Conversation the HNW Client Has Never Had

The technology entrepreneur I described at the opening of this article told me, at the end of our second meeting, that in thirty years of financial life he had never had this conversation. He had had the income replacement conversation many times. He had always politely declined. He had never been asked what percentage of his portfolio was guaranteed, or how much disruption his family could absorb, or whether the structure of his estate would survive a two-year probate process.

Those three questions opened a conversation that changed his planning entirely. Not because I persuaded him to buy a product. Because I showed him a genuine gap in his portfolio, a gap he had never seen because nobody had framed it that way, and offered him the right tool to fill it.

The HNW insurance conversation is not about convincing clients they need protection. It is about showing clients a problem their portfolio has that they have never seen presented in a language they recognise. The moment you speak their language, portfolio certainty, estate engineering, structural liquidity, you are no longer the insurance advisor. You are the most useful person in the room.

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.