Insurance as Portfolio Strategy

Speaking the Language of the Investment-Savvy HNW Client

I have been in enough client meetings to know exactly how the conversation dies. An advisor has spent twenty minutes building rapport with a sophisticated investor, hedge fund background, private equity, a portfolio that has returned 14 percent over the past decade. And then the advisor says: "I would also like to talk to you about your insurance needs."

The client's demeanour changes almost imperceptibly. Not hostile, just subtly disengaged. The advisor has just categorised themselves. They are no longer a peer having a strategic conversation about capital. They are a product salesperson who has pivoted to their pitch. The client is polite. But the real conversation is over.

This is the most preventable failure mode in HNW financial planning. It is not caused by the product. It is caused by the language. The product that was about to be discussed, whole life, endowment, PPLI, may have been precisely the right strategic instrument for that client's portfolio. The language that introduced it signalled the wrong framing entirely.

This article is about the language shift. It explains how financial planners can present insurance-based structures to investment-sophisticated HNW clients not as protection products but as portfolio instruments, using the vocabulary that sophisticated investors already think in, and addressing the problems that sophisticated investors already have.

Why Investment-Sophisticated Clients Resist the Standard Insurance Conversation

The resistance is not irrational. It is the logical response of someone who thinks in terms of risk-adjusted returns, portfolio construction, and capital efficiency hearing a conversation framed in terms of protection and beneficiaries. These are different intellectual frameworks. The protection framework assumes the client is worried about dying. The portfolio framework assumes the client is worried about capital efficiency, estate transfer cost, and structural risk. The second set of concerns is far more resonant for a client who has already solved the problem of financial survival.

The insight that changes everything is this: structured insurance addresses problems that every sophisticated investor's portfolio has. It addresses them better than any alternative instrument. And it does so in a way that is structurally complementary to the rest of the portfolio, not a replacement for equities or property, but the allocation that fills a gap that no equity, bond, or property position can fill.

The four concepts below are the language shifts that open this conversation with investment-sophisticated HNW clients. Each one takes an idea the client already understands from their investment experience and shows them the insurance structure through that lens.

Four Concepts That Reframe Insurance as a Portfolio Tool

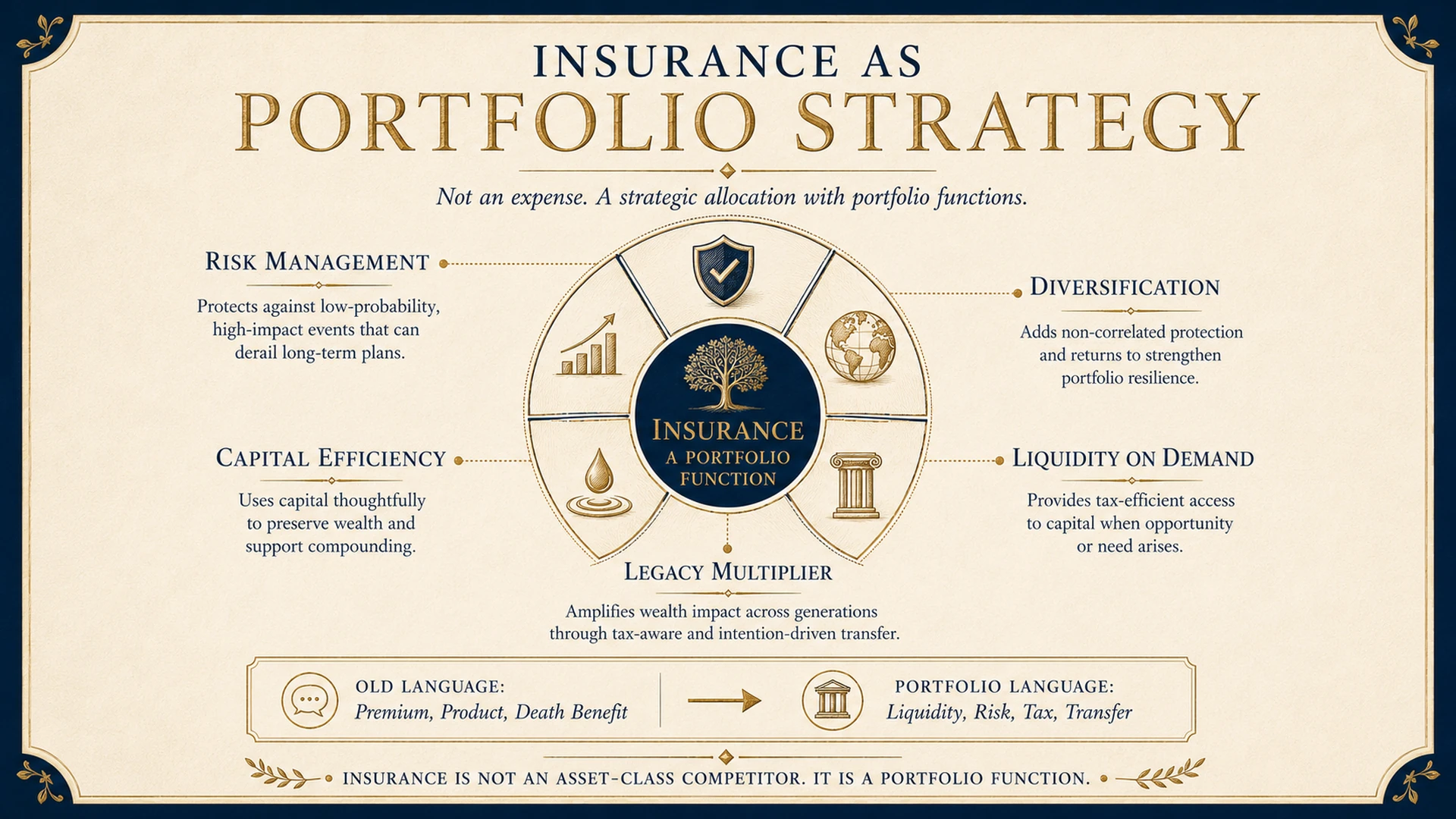

The missing allocation. Every sophisticated investor understands that a well-constructed portfolio allocates across asset classes, equities for growth, bonds for income, property for tangible value, cash for liquidity. The conversation that works with HNW clients is not 'you should have insurance.' It is: 'In your portfolio right now, what percentage of your assets is contractually guaranteed, not likely to grow, not historically stable, but guaranteed regardless of market conditions?' For most sophisticated investors, the answer is very little or none. That gap, the absence of guaranteed capital certainty in the portfolio, is the opening. Structured insurance is the allocation that fills it. It does not compete with equities or property. It serves a function that nothing else in the portfolio serves.

The put option. For the client who manages downside risk in their investment portfolio using options strategies, the put option framing is immediately understood. A put option gives the holder the right to a predetermined minimum value regardless of how the underlying asset performs. The premium is the cost of removing tail risk. Insurance is the put option on the client's most important asset, their life and the capital it represents. The death benefit is always in-the-money. The premium is the cost of contractual certainty. And unlike market options, this particular put option does not expire, and after twenty years, the premium returns. The conversation is not about protection. It is about intelligent risk management on the primary asset in the portfolio.

The shock absorber. The finest portfolio in the world, growing at 12 percent per annum, will be disrupted by an unstructured estate transition. Probate delays of 18 months, forced asset sales to fund estate duties, liquidity crises at the moment the family is least able to manage them, these are not hypothetical risks. They are documented outcomes that destroy a significant fraction of the accumulated value. The shock absorber framing asks the client: your portfolio is a high-performance vehicle, what are the shock absorbers? A premium car is not faster than an ordinary one because of its shock absorbers. It is more composed. It delivers the same performance over rough roads without transferring the disruption to the driver. Structured insurance in the portfolio keeps the estate transition composed regardless of what is happening in the markets when it occurs.

The capital preservation lock. For the HNW client who has reached the stage of asking 'I have built enough, now how do I make sure I do not lose it?', the ratchet framing is the most resonant. A ratchet allows movement in one direction only. Forward progress is locked in. Backward movement is mechanically prevented. Every other asset class in a sophisticated portfolio can go backwards: equities fall, property markets correct, business valuations fluctuate. A properly structured whole-life or endowment allocation is the ratchet, the portion of the portfolio whose value cannot go backwards, regardless of market conditions, and which transfers to the next generation at its guaranteed value. It does not grow as fast as equities. It is not meant to. It is meant to lock in a portion of accumulated wealth permanently.

The Language Table: What to Stop Saying and What to Start Saying

Table 1. The Language Shift for Investment-Sophisticated HNW Clients. The left column signals a product sale. The right column signals a strategic planning conversation.

The product is the same. The language is the difference. When a client hears 'insurance,' they hear 'expense.' When they hear 'put option,' they hear 'intelligent risk management.'

Three Practical Steps for Financial Planners

Lead with the portfolio gap question, always. Before any concept is introduced, before any product is mentioned, ask: 'What percentage of your current portfolio is contractually guaranteed regardless of market conditions?' This question puts the client in their own intellectual framework, portfolio construction, and creates the opening for insurance as a strategic instrument without ever using the word insurance to introduce it.

Match the concept to the client's primary concern. Investment-sophisticated HNW clients have specific concerns that cluster around four themes: portfolio completeness, downside risk management, estate transfer efficiency, and capital preservation after they have 'won the game.' Match the concept to the concern. The put option framing works best for risk management conversations. The missing allocation framing works best for portfolio completeness conversations. The capital preservation lock works best for clients who are already wealthy and primarily focused on not losing what they have.

Never introduce all four concepts in one meeting. Each concept is a door. Pick the door that matches where this particular client is standing and open it. A client who is managing a USD 200 million portfolio with an options overlay does not need the missing allocation concept, they need the put option framing. A client who just sold a business and is asking how to protect the proceeds needs the capital preservation lock. Matching concept to client is what separates a strategic conversation from a product presentation.

The Advisor the HNW Client Has Been Waiting For

The investment-sophisticated HNW client is not resistant to insurance-based structures. They are resistant to conversations about insurance that treat them as though they are buying a protection product rather than making a portfolio decision. The moment the conversation shifts to the right frame, portfolio completeness, risk management, estate efficiency, capital certainty, the resistance dissolves.

The financial planner who can make that shift fluently, who can sit across from a sophisticated investor and have a peer conversation about portfolio construction that happens to conclude with a structured insurance allocation, is providing a service that investment managers, private bankers, and tax advisors cannot. They are speaking the client's language, addressing the client's actual concerns, and offering a solution that fits the client's mental model of how their wealth should work.

Building the Habit: One Question Before Every HNW Meeting

The language shift described in this article is not a technique to deploy once and then return to the standard approach. It is a habit, a discipline of framing that, once established, becomes the natural way of opening every HNW conversation.

The habit begins with one question, asked of yourself before every meeting with a sophisticated investor: what does this client's portfolio currently lack that no equity, bond, or property can provide? The answer is almost always the same, guaranteed capital certainty, liquidity at a defined moment, tax-efficient transfer. But the way that answer is expressed in the meeting should be specific to this client's situation, this client's vocabulary, and this client's primary concern at this stage of their wealth journey.

The portfolio gap question, the put option framing, the shock absorber analogy, the capital preservation lock, these are not a menu to work through systematically. They are tools to deploy selectively, based on what the client has told you matters most. The planner who listens carefully before speaking is the one who chooses the right tool for this particular person at this particular moment. And that precision, that sense of being genuinely understood rather than generically advised, is what creates the trust that sophisticated investors reserve for very few people.

Start with the gap question. Listen to the answer. Build from what the client tells you. The language shift follows naturally from genuine attention, and genuine attention is something no product presentation can replicate.

That is the advisor the HNW client has been waiting for. The language shift is how you become them.

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.