From Assets to Legacy

How to Help Clients Build a Wealth Structure That Outlives Them

There is a question I ask near the end of almost every first meeting with a new client. Not during the fact-find, not during the balance sheet review, not during the insurance audit, but at the end, when the numbers have been laid out and the structure has been discussed and there is a moment of quiet. The question is this: what do you want your wealth to do for your family?

Not how you want it divided. Not which jurisdiction is most tax-efficient. Not how to minimise the estate duty. What do you want it to do?

Most people pause. Some look surprised, as if the question caught them off-guard in a meeting they thought was about spreadsheets. And then, almost always, they give an answer that has nothing to do with money. They want their children to have security. They want their grandchildren to have choices they did not have. They want the family to stay close. They want their values to outlast them.

These are not financial goals. They are human ones. And they are, in every meaningful sense, the real purpose of everything the client has been building. Most wealth structures are designed to protect assets. The best ones are designed to protect intentions. The gap between those two objectives is where legacies are lost.

This article is about closing that gap, about the specific steps a financial planner can take to help HNW clients build a wealth structure that does not merely preserve assets but genuinely carries the client's intentions forward across generations.

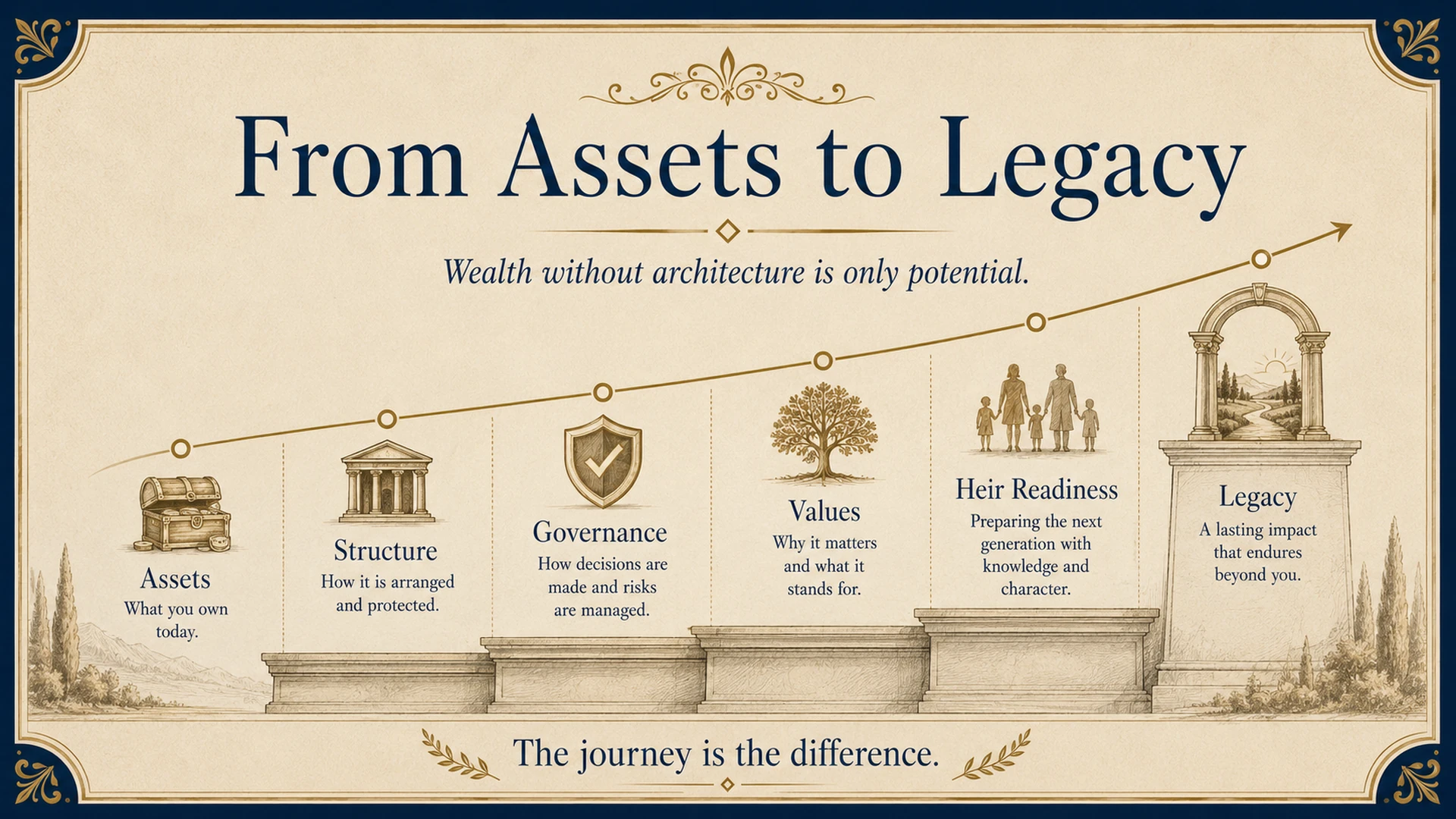

The Legacy Equation: Three Elements That Must All Be Present

A lasting legacy is not an accident. It is not the natural consequence of accumulating enough wealth. In my experience working with multi-generational families across the GCC, Southeast Asia, and South Asia, every family whose wealth has genuinely endured has had three things in alignment. Every family that has lost it was missing at least one.

Values, the principles and priorities the founder wants to preserve across generations. These are not abstract ideals. They are specific answers to specific questions: what is this wealth for? What should it enable? What should it prevent? How should family members behave toward each other and toward the world when they are the stewards of this wealth? Values that are never articulated cannot be transmitted. Values that are never documented cannot outlast the person who held them.

Wealth, the resources to sustain the family's aspirations and philanthropic goals across time. This is the dimension that financial planning addresses most naturally, growth, preservation, tax efficiency, income planning. But wealth without values produces heirs who are materially comfortable but purposeless. And wealth without structure produces good intentions that dissolve at the first disagreement.

Structure, the tools and systems that ensure both values and wealth endure. Discretionary trusts that release funds according to conditions the founder defined. A family constitution that documents the governance framework and the family's shared commitments. A philanthropic programme that aligns the family's giving with its values and engages each generation in meaningful stewardship. A coordinating advisor who ensures all these elements remain current and coherent.

Remove any one of these three, and the legacy fractures. Wealth without values produces purposeless heirs. Values without wealth cannot sustain themselves. And wealth combined with values, without structure, depends entirely on the ongoing goodwill and alignment of individual family members, which history consistently shows is a fragile foundation.

The Intergenerational Bank Balance: Knowledge and Wealth Together

One of the most powerful frameworks I use with clients is what I call the Intergenerational Bank Balance, the idea that a genuine legacy consists of two accounts, not one: a money bank and a knowledge bank.

The money bank is straightforward: the assets, the structures, the legal arrangements, the insurance, the investment portfolio. This is what most estate plans address. The knowledge bank is everything else: the family's story, the origin of the wealth, the values and principles that shaped the decisions that built it, the lessons of failure and success, the relationships and networks that gave the family its position.

I have seen two families with similar levels of wealth navigate the same generational transition with completely different outcomes. The first family left behind a substantial money bank with no knowledge bank. The heirs inherited assets they had never been prepared for, values that had never been articulated, and decisions that had never been explained. Within a decade, the wealth was gone. Not from recklessness, from a series of individually defensible decisions made without a compass.

The second family did something different. Alongside the legal structures, the patriarch documented his journey: the warehouse he built at twenty-six with borrowed money, the deals that went wrong and what he learned from them, the relationships that mattered and why, the principles he had always used to make difficult decisions. His children had been listening to those stories for years. By the time they inherited, they were not overwhelmed. They were prepared.

Wealth without values is fleeting. Values without wealth lack reach. But together, they are unstoppable., Dr. Sanjay Tolani

Three Tools That Build the Legacy Layer

Discretionary trusts as legacy instruments. The most powerful inheritance planning tool for legacy building is the discretionary trust, not because of its tax efficiency, which is significant, but because of its capacity to carry the founder's intentions with precision. A well-drafted discretionary trust can release funds at specific life stages, for specific purposes, with specific conditions attached. It protects the family from external threats, creditors, divorces, poor decisions, while preserving the founder's vision of what the wealth is for. The conversation to have with every HNW client is: if you could design the exact conditions under which your grandchildren access this wealth, what would those conditions be? The answer to that question is the trust deed.

The family constitution as the governance anchor. A family constitution is a living document that defines who the family is, what the family values, how the family makes decisions, and how the family resolves disagreements. It is not a legal instrument, it is a shared commitment. A well-drafted constitution covers the family's mission statement, the governance structure, the role of professional advisors, the process for admitting new family members, the family's approach to philanthropy, and the process for resolving disputes before they become legal proceedings. The Lim family I worked with in Singapore reviewed and updated their family constitution every three years. The review process itself became a family ritual, a moment of reconnection around shared purpose that proved more valuable than the document.

Structured philanthropy as a values transmission system. Philanthropy in HNW planning is often discussed in tax terms, donor-advised funds, foundations, deductions. These are real benefits. But the more powerful reason to structure a family's giving is the values transmission that structured philanthropy creates. A family that gives together around shared causes, that tracks its giving against defined outcomes, that involves each generation in the direction of its philanthropic programme, is a family that keeps its values active and visible across generations. The child who allocates charitable grants at fifteen has a fundamentally different relationship to wealth stewardship at thirty-five than the child who receives a cheque without any involvement.

Three Practical Steps for Financial Planners

Ask the legacy question in every first meeting. Not near the end, in the middle, when the human being across from you is present and engaged. 'What do you want your wealth to do for your family?' Record the answer carefully. It should govern every planning recommendation that follows.

Audit the knowledge bank, not just the money bank. When reviewing a client's wealth structure, ask explicitly: has the family's story been documented? Have the founder's values been written down? Do the heirs know why the wealth exists and what the founder wanted it to achieve? If the answer to any of these is no, the legacy plan is incomplete regardless of how well-structured the trust deeds are.

Introduce the family constitution as the missing piece. Most HNW clients have legal structures, wills, trusts, shareholder agreements. Very few have a family constitution. Positioning the family constitution as the document that makes the legal structures coherent, the governance layer that connects all the other pieces, gives financial planners a concrete deliverable that goes well beyond any product or investment recommendation.

The Wealth That Stays

The families I have seen preserve their wealth across generations are not the ones with the most sophisticated tax structures. They are the ones whose children understood why the wealth existed and felt personally responsible for its continuation. That understanding, that sense of stewardship, is never created by a trust deed alone. It is created by the stories that get told, the values that get modelled, the conversations that happen at the dinner table over years, and the governance structures that make those values binding across generations.

When the Structure and the Story Finally Align

One of the most moving experiences in my practice occurs when a client, usually a patriarch or matriarch in their sixties or seventies, with wealth they have spent their whole life building, finally completes this work. The structures are updated. The family constitution is signed. The philanthropic programme is running. The trust releases funds in stages aligned to the values they articulated. The heirs know the story.

There is a specific kind of conversation that becomes possible only at that point. It is no longer a conversation about protection or planning. It is a conversation about purpose. About what the family stands for, what it wants to build next, and how the wealth that has already been accumulated can be put to work in the service of something larger than its own preservation.

I have seen families reach that conversation after years of doing this work together, and I have watched the relief it produces in the person who built the wealth. Not because the structure is complete. But because for the first time, they can see that what they built will not just survive them. It will carry their intentions forward long after they are gone.

That outcome does not come from a product or a structure or a tax strategy. It comes from a financial planner who was willing to ask the human question first, who held the full picture when no one else would, and who built the knowledge bank alongside the money bank. That is the work this article is calling you to.

The financial planner who helps a client build the knowledge bank alongside the money bank, who helps define the values, design the governance, and structure the philanthropy, is doing work that no other professional will do. And they are building a relationship that lasts not for the length of one client's life, but for the length of the family's.

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.