Does Your Client Actually Need a Family Office?

A Practical Decision Framework for Financial Planners

One of the most consistent patterns I have observed across more than two decades of practice is that the term 'family office' means entirely different things to the people who use it. I have heard it used to describe a three-person team managing USD 800 million for a single dynasty family in Singapore. I have heard it used to describe one part-time bookkeeper and a shared spreadsheet managing USD 15 million for a patriarch who prefers not to think about these things. I have heard clients say they have a family office when what they mean is that their private banker sends a quarterly report, and I have heard clients say they do not have a family office when what they are describing, a coordinated team of specialists aligned around a shared advisory mandate, is precisely what a well-functioning family office is.

This definitional confusion has a practical cost. Families that need a family office and do not have one accumulate structural drift, the quiet misalignment of legal, tax, insurance, and governance layers that produces expensive consequences at transition events. Families that have something they call a family office but that does not function as one pay the costs of an institution without receiving its benefits. And families that would be better served by a coordinated specialist network continue paying for a dedicated infrastructure that delivers less value than the overhead consumes.

This article gives financial planners a practical framework for answering the question that clients almost never ask but almost always need answered: what kind of wealth governance structure does my family actually need right now, and what does it need to become?

What a Family Office Actually Does

Before advising a client on whether they need a family office, it helps to be precise about what a family office is, not the institutional mythology, but the functional reality.

A family office is a coordinating function. At its most fundamental level, it exists to ensure that all the specialist advisors serving a wealthy family, the investment manager, the tax advisor, the estate attorney, the insurance specialist, the corporate secretary, are working from the same picture of the family's goals, and that their recommendations are aligned rather than contradictory. That is the core function. Everything else, the investment platform, the accounting infrastructure, the philanthropy management, the lifestyle services, is built on top of that coordinating mandate.

The most common failure mode in HNW wealth management is not bad advice from any single advisor. It is good advice from multiple advisors that, in combination, produces incoherent outcomes. The attorney structures the trust for estate tax efficiency. The financial planner allocates the portfolio without reading the trust's distribution terms. The insurance specialist places the policy without knowing that the trust was amended six months earlier. The tax advisor files the returns without knowing about a cross-border asset acquisition. Each individual recommendation is defensible. Together, they create structural friction that accumulates, year by year, until a transaction or a transition event makes the friction visible, at great cost.

The family office, properly understood, is the infrastructure that prevents that friction. Whether it needs to be a dedicated institution with full-time staff, a shared infrastructure serving multiple families, or a coordinated network of specialists linked by a central mandate depends entirely on the scale and complexity of the family's situation.

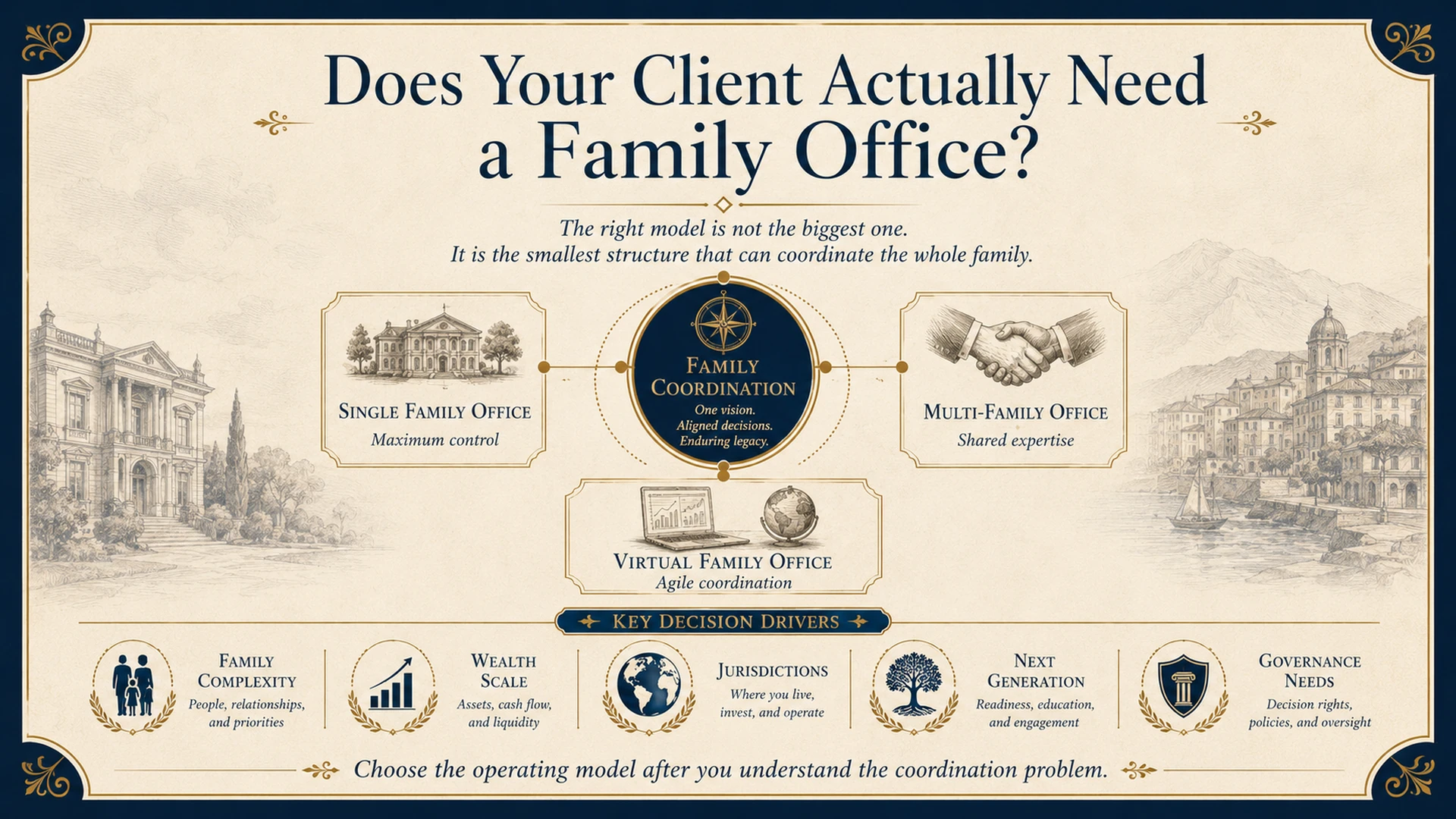

The Three Models: SFO, MFO, and Virtual

Family offices exist on a spectrum with three recognisable models, each appropriate for a different combination of wealth scale, complexity, and governance preference.

Table 1. The Three Family Office Models. The right choice depends on wealth scale, complexity, jurisdictional footprint, and governance preference, not on what sounds most prestigious.

The most expensive family office decision is not choosing the wrong model. It is having no coordinating function at all, because the cost of structural drift from uncoordinated advisors accumulates invisibly until a transaction forces it into view.

The Decision Framework: Five Questions That Determine the Right Model

In practice, the right family office model for a client can be determined by working through five questions. The answers do not produce a formula, but they consistently point toward the appropriate structure for the family's current situation, and toward the moment when that structure needs to evolve.

What is the total net worth and how is it distributed? Families with net worth below USD 20 million are typically well-served by a coordinated specialist network, the equivalent of a VFO, rather than by any formal family office structure. Families between USD 20 and USD 100 million are typically best served by an MFO or a well-structured VFO with a dedicated coordinator. Families above USD 100 million begin to approach the threshold where a dedicated SFO infrastructure starts to deliver value commensurate with its cost. These are guidelines, not rules, a USD 50 million family with assets in seven jurisdictions may need more institutional infrastructure than a USD 150 million family concentrated in a single market.

How many jurisdictions does the family touch? A family concentrated in a single jurisdiction can be well-served by a coordinated local advisory team. Each additional jurisdiction adds layers of compliance, legal complexity, and potential structural conflict that require specialist knowledge that no single advisor or generalist platform can cover. Families in three or more jurisdictions almost always benefit from a coordinator whose explicit mandate is to ensure cross-jurisdictional alignment, which is the core function of the VFO model, regardless of whether the family has the scale for a full SFO.

Is there an active business in the structure? Families with active operating businesses face a governance challenge that purely financial families do not: the line between personal and business governance is porous, succession and exit planning require dedicated attention, and the family office must be able to engage with the business's advisors as well as the family's personal advisors. An SFO or MFO with genuine corporate advisory capability is significantly more valuable for these families than a platform focused primarily on investment management.

How many generations are currently active? A family in which only the founding generation is active can be served with relatively light institutional infrastructure. A family with three generations simultaneously involved in governance, where G1 is still active, G2 is leading, and G3 is being prepared, has a governance complexity that requires systematic processes for decision-making, role definition, and knowledge transfer. This multi-generational governance challenge is one of the strongest indicators that a formal family office structure, SFO, MFO, or a highly structured VFO, adds genuine value beyond what an informal advisory arrangement can provide.

Is there a coordinator who holds the full picture? This is the most diagnostic question. Regardless of what the family calls their advisory arrangement, the test of whether it functions as a family office is simple: is there one person who can describe, in precise detail, every significant asset, every legal structure, every insurance policy, every compliance obligation, and every governance document that the family has, and who has the mandate to ensure that all of these are aligned? If the answer is yes, the family has a functional family office regardless of what it is called. If the answer is no, the family does not have a functional family office regardless of how impressive the institutional name on the letterhead might be.

The Ferreira Lesson: What Happens Without a Coordinator

The cost of not having a functional coordinating function is not theoretical. The Ferreira family, a third-generation Brazilian-Portuguese family with assets across three jurisdictions, sold a significant portion of their business in 2021. They had advisors in each jurisdiction. They did not have a coordinator who held the full picture.

The result was USD 8.5 million in avoidable costs: a tax liability significantly larger than necessary because a structural reorganisation that would have reduced it had been discussed but never executed, US estate tax exposure created by a 2018 advisory recommendation that was never integrated with the broader structure, and cross-jurisdictional conflicts between the Portuguese and Brazilian succession regimes that had existed for years but had never been identified because no one had been tasked with looking across both simultaneously.

At the conclusion of the remediation, the Ferreira patriarch said something I have quoted many times since: "We paid eight and a half million dollars to understand why this matters. You are now offering us the same lesson for considerably less. I would encourage whoever reads this to take the cheaper path."

The cheaper path is a coordinator with the full picture, whatever the institutional form around that role. For some families, that means establishing an SFO. For others, it means joining an MFO. For many, particularly those who are globally mobile and jurisdictionally complex, it means establishing a VFO with a dedicated Asset Structuring Expert at the centre, supported by a specialist network that covers every domain the family requires.

The Role Financial Planners Can Play

For financial planners who advise HNW clients but do not manage a family office, the practical opportunity in this framework is the coordinator role itself. The financial planner who takes on an explicit mandate to hold the full picture, to ensure that the attorney, the tax advisor, the insurance specialist, and the investment manager are aligned, to convene annual reviews that cover all domains simultaneously, and to be the professional who is called first when any significant event occurs, is performing the core function of a family office regardless of what it is called.

This role is undervalued and underpriced in most financial planning practices, because it is not directly tied to a product sale or an AUM fee. But it is the most durable, most relationship-deepening, and most genuinely valuable service that a financial planner can offer an HNW client. Families do not change their coordinator lightly. A planner who occupies this role with competence and integrity occupies it for decades.

The question to ask in the next HNW client review is straightforward: who holds your family's full picture? Who knows what every advisor has recommended, and ensures those recommendations are aligned? If the honest answer is 'no one,' you have just identified both the gap and the opportunity.

Read the research behind the framework.

Get the 37-page Tolani Family Office research paper on Private Placement Life Insurance, purpose, advantages, §7702 compliance architecture, and the Tolani Flow® model. Free.